With just five weeks until what will be a very different Christmas this year, this Clear Digital Digest examines:

LOCKDOWN 2.0 Although not the cheeriest subject, this is the first Clear Digital Digest since we went into a second lockdown on 5th November.

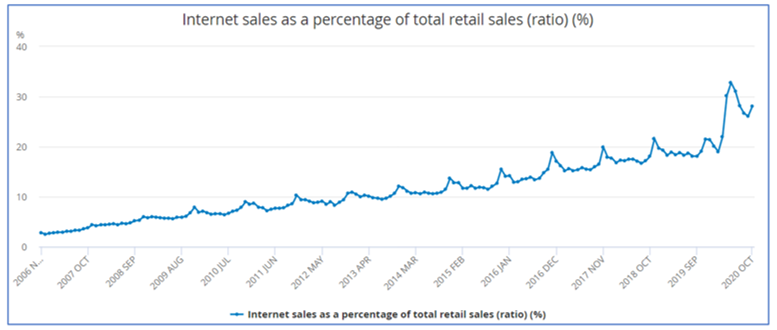

Source: ONS BLACK FRIDAY: ONE WEEK TO GO As well as the lockdown, online sales in November will be further boosted to some degree by Black Friday next week.

DELIVERY: SANTA WILL BE INCREASINGLY BUSY THIS YEAR One topic that we will likely hear more about in the coming weeks is the problems caused by these inflated online sales when it comes to actually delivering the orders.

CHRISTMAS ADVERTISING Of course, to many it wouldn’t feel like Christmas without the high prestige TV led campaigns we are now accustomed to expect, which have really increased in profile over the last week with the launch of both the John Lewis ad plus a new series of ITV ratings winner “I’m A Celebrity Get Me Out Of Here”.

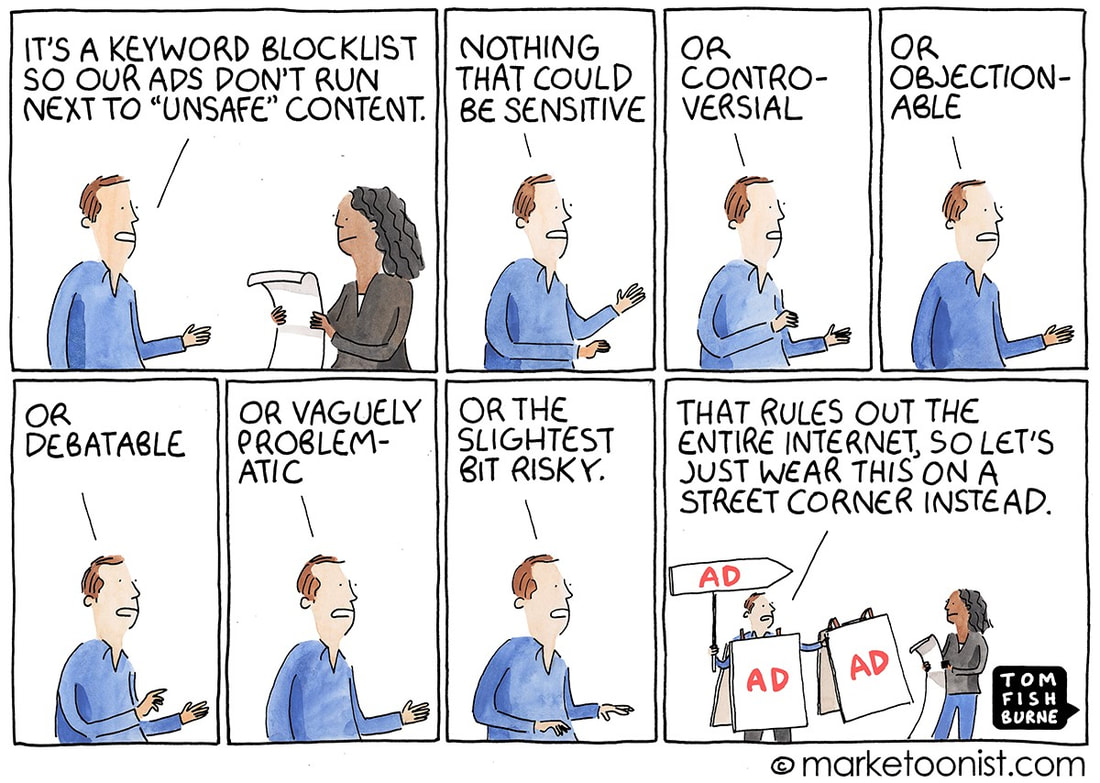

AND FINALLY… As alluded to above, forecasting accurately for 2021 is going to pose more challenges than for any year in living memory. So I liked this take on strategic planning from Tom Fishburne, the ever entertaining Marketoonist…

0 Comments

Clear Digital Digest: subscription coffee, Amazon ads, retail sales update and cricket data18/9/2020  Today’s Clear Digital Digest looks at some recent stories regarding Pret A Manger and Amazon, reviews today’s new ONS retail data and learns how the data revolution is transforming the world of cricket.

PRET A MANGER: ALL YOU CAN DRINK

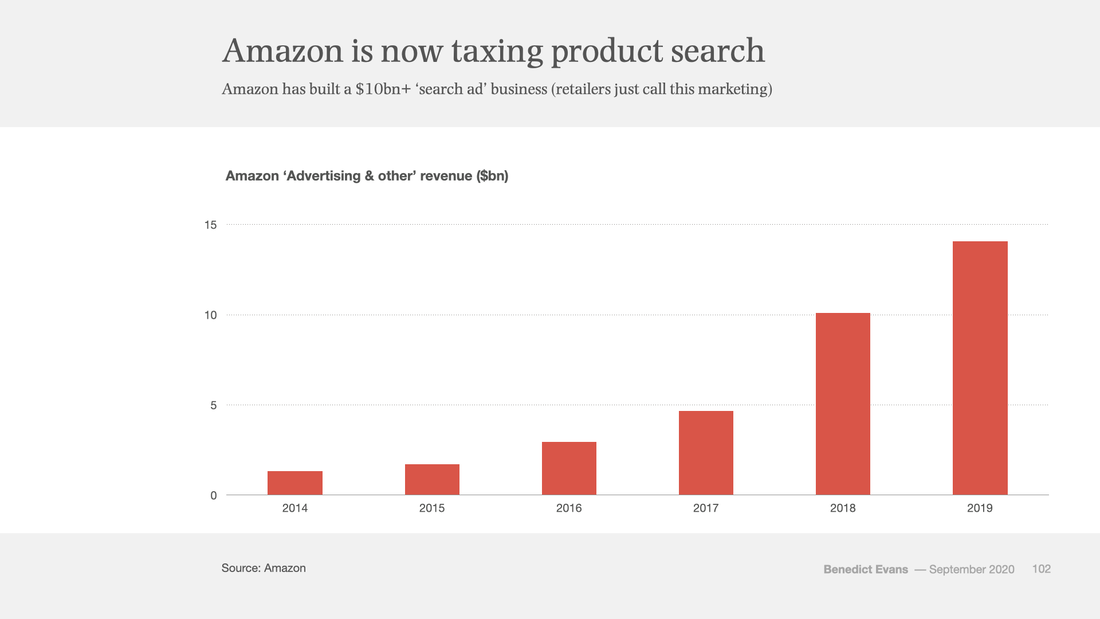

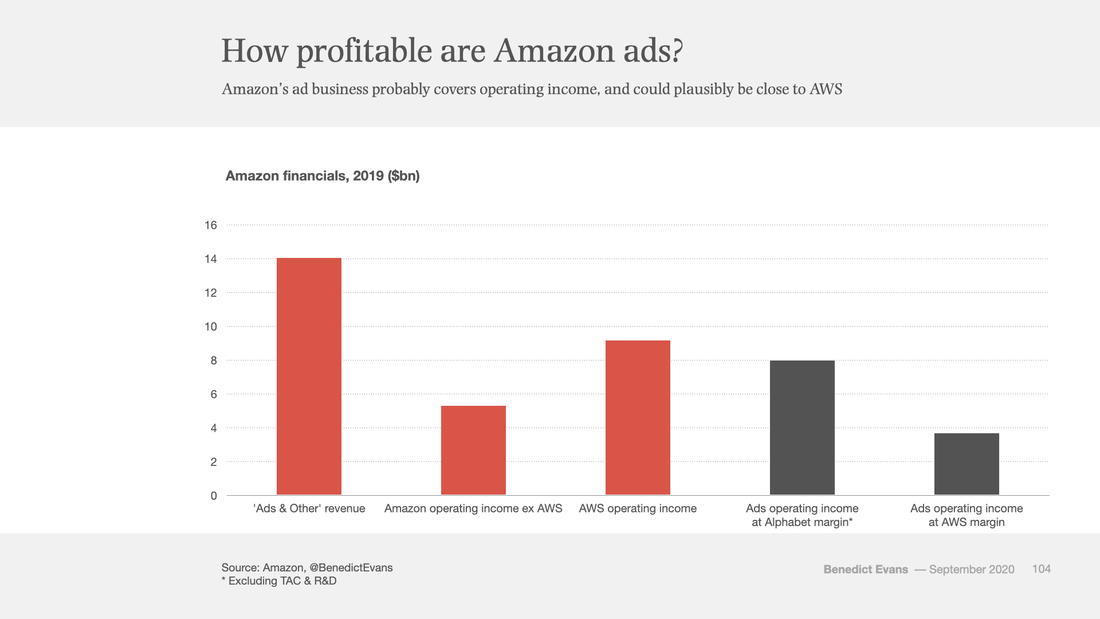

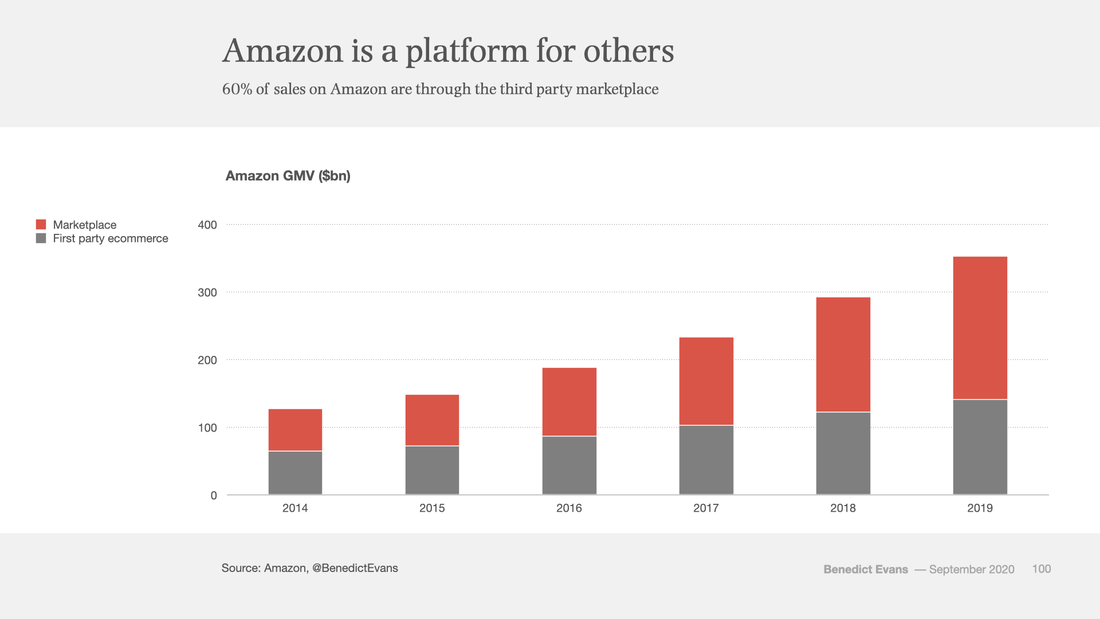

AMAZON’S PROFITABILITY: INCREASINGLY DRIVEN BY ITS ADVERTISING Well worth a read is this fascinating article about Amazon and its profitability, courtesy of Ben Evans.

RELEASED TODAY: ONS RETAIL SALES UPDATE FOR AUGUST The Office for National Statistics (ONS) have today released their latest retail sales figures for August. We reviewed July’s data in a Digital Digest last month, so here’s a quick update, one month on…

AND FINALLY... When my subscription copy dropped through my letterbox this week, I was surprised to see The Cricketer magazine (now in its centenary year) highlighting “The Data Decade” on its front page.  With the relevant articles exploring how increasing use of digitised data has fundamentally changed recent cricket coverage and some future predictions on how this may evolve, it’s a timely reminder than even such a traditional pastime as cricket is experiencing unprecedented change with its own digital/data revolution.

But this also demonstrates that there is still a place for more traditional media…yes I do still read some print magazines as well…  Today’s Clear Digital Digest round-up looks at:

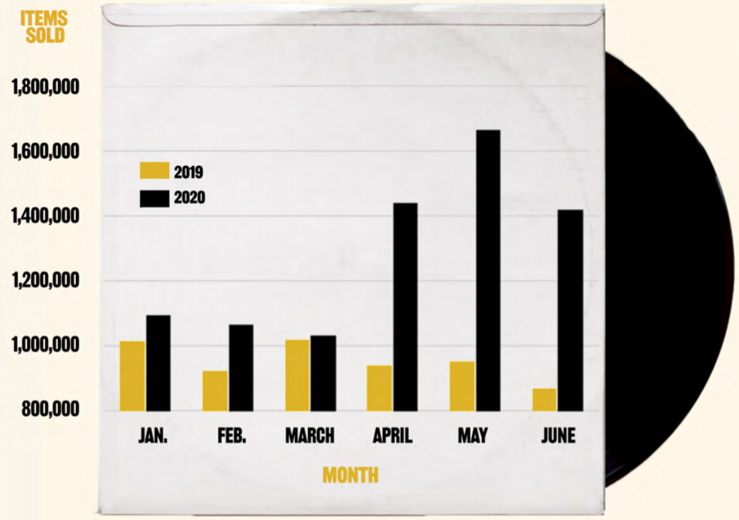

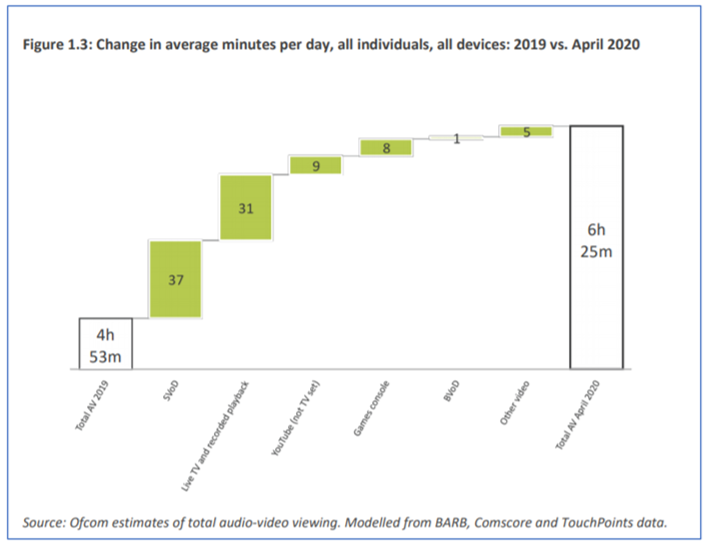

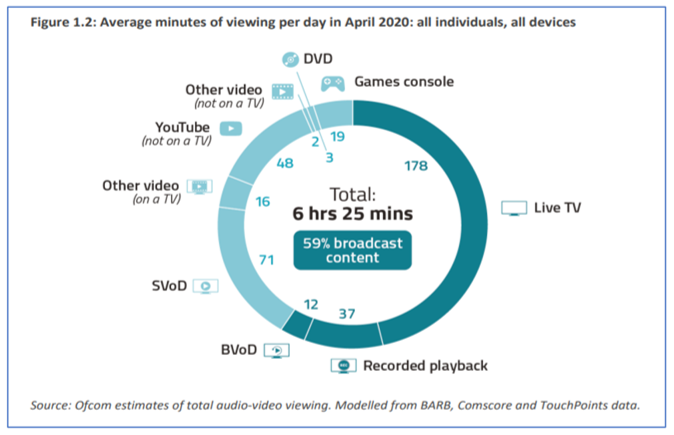

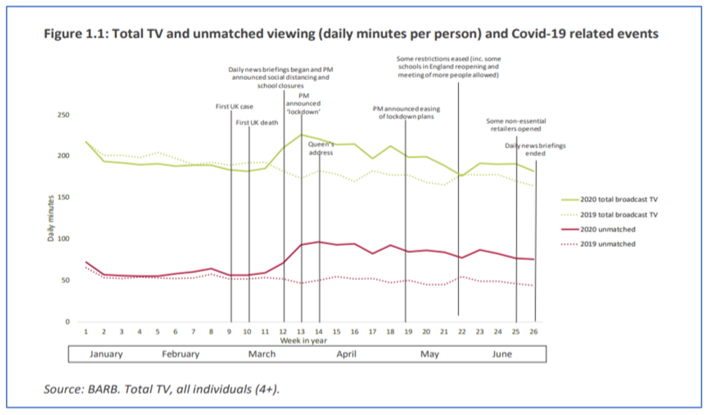

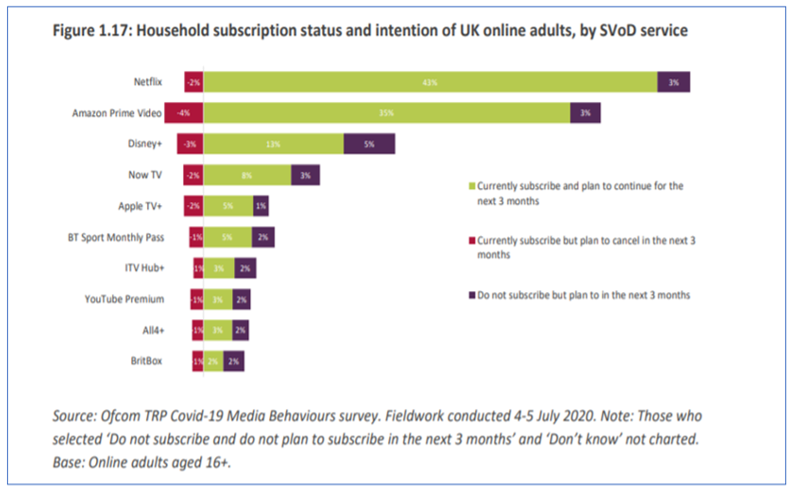

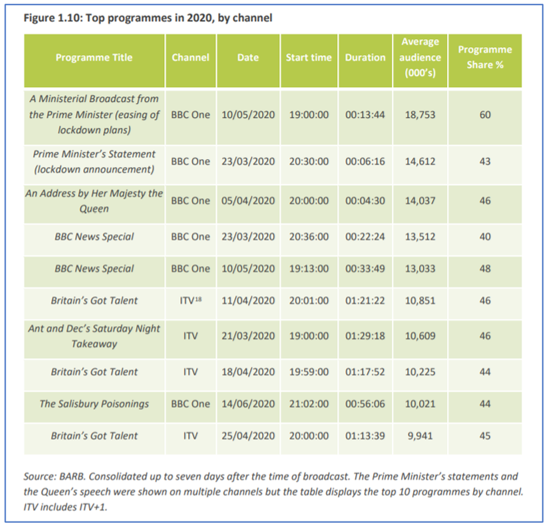

OCADO LAUNCHES WITH MARKS & SPENCER: PERCY PIGS FOR ALL (WELL, SOME…)  Ocado launched their much publicised partnership with Marks & Spencer on Tuesday (Percy Pig branded vans et al) and with such a highly anticipated launch, perhaps unsurprisingly there were teething troubles as some disgruntled customers were not happy that their day one orders were cancelled. Those of us who have been around the block won’t be surprised that there were one or two problems with a new service launch, and time will tell how short-term or significant these issues were. However, Ocado chief executive Tim Steiner was perhaps bullishly tempting fate the weekend before when he told the Sunday Times: “They [Waitrose] have done an advert saying ‘we’ll take it from here’ or something. Well, they can’t take it from here because they don’t have the technology, the infrastructure or the systems.” “Taking it from here” referred to the fact that previous Ocado partners Waitrose were already running their own parallel Waitrose.com delivery service, generally despatched from local Waitrose stores rather than Ocado’s regional distribution hubs. Waitrose also recently announced plans for a 12 week trial with Deliveroo, joining brands such as Morrisons and the Co-Op already on the platform in selected locations. Sainsburys also continue to expand and promote their similar new ChopChop service, as the choice and variety of grocery home delivery options expands to keep up with this year’s step change in customer demand. VINTAGE/USED ITEMS CONTINUE TO DRIVE SALES ON EBAY AND DISCOGS There were two updates from key marketplaces this week, both showing the increasing appetite for vintage/second hand items, a trend we explored in much more depth in our recent deep dive on “The UK Marketplace Sector – And The Role Of Community”. eBay UK have stated that sales of used goods jumped 30% between March and June this year leading to an overall 10% rise in the first half of 2020 compared with last year. Secondhand and vintage fashion is by far their biggest category, but sales of secondhand chairs, sofas and TVs also shot up by 41%, 30% and 17% respectively during June and July compared with February and March. Music community Discogs (the 10th most visited marketplace in the UK) have also released their mid-year report this week. In the first six months of 2020, 4.3m orders were placed globally through the Discogs marketplace (+30% year on year) for a total of 7.7m items (+34% YOY). Vinyl records remain by far the largest sellers for Discogs, with 5.8m sold (+34% YOY) although CD sales also grew by a similar amount, with 31% YOY growth for the 1.7m sold.  Total items sold by month on Discogs H1 2020 v 2019 (Source: Discogs) As the chart above shows, Discogs sales growth really accelerated as lockdown fully kicked in around the world, although January and February were already showing healthy sales growth. This is in line with more recent trends for Discogs, who sold a total of 14.6m records in 2019, growing by 34% on 2018. We explored the Discogs marketplace – and the community that underpins it – in more detail in our recent deep dive “Discogs: The Digital Success Story Of The Vinyl Revival”. NETFLIX TRIALS FREEMIUM  Netflix this week revealed plans to offer some of its original movies and shows to non-subscribers. Free films available include Bird Box and The Two Popes, while original series include Stranger Things and Our Planet. The real hook to this new initiative is the fact that it’s only the first episode of each show that is available, although Netflix newbies can still get a month’s free trial to then continue watching. This type of freemium model seems to make perfect sense for a lower risk trial for anyone that hasn’t yet succumbed to Netflix’s charms; as we reported last month, 43% of UK households currently subscribe to Netflix, ahead of Amazon Prime Video’s 35%. A full list of “free” Netflix shows and movies is available here. AND FINALLY... In a week when the future of another certain Argentinian footballing genius remains up in the air, this tweet raised a chuckle (and makes perfect sense with the final touch)…   Today’s Clear Digital Digest reviews a recent Ofcom report about our changing TV and video viewing habits since lockdown. We also take a look at changes in the ecommerce world, covering both shopper attitudes plus news from Amazon, Aldi and the mooted return of a familiar old retail brand, Comet… CHANGING VIEWING HABITS Ofcom have just released their latest annual Media Nations research report, examining how we consume TV, video, radio and audio content. This year’s events have unsurprisingly seen quite significant changes since March, so Ofcom have added two chapters to their report examining Covid-19 related trends. Some key highlights from this are:

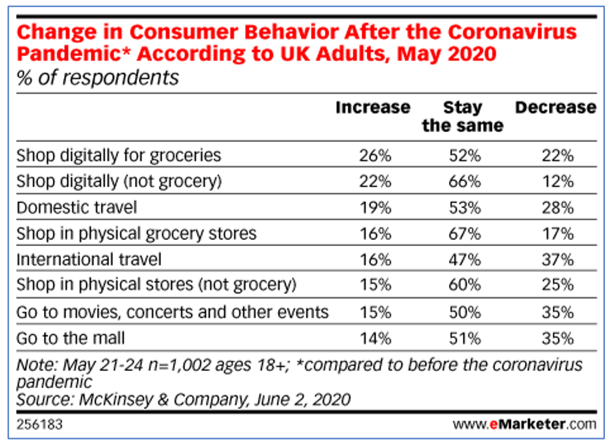

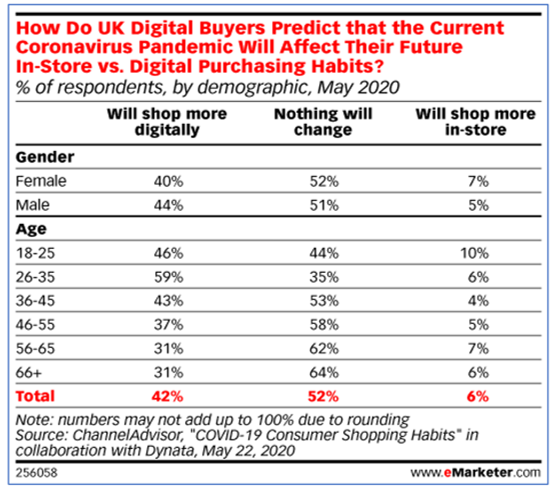

CHANGING SHOPPING HABITS As well as changing our viewing habits, Covid19 has also fundamentally changed our shopping habits with the well documented growth in online shopping. eMarketer have taken a look at what these shifts may mean in the longer term.

Looking at other ecommerce stories, a week never seems to go by without some significant Amazon news and the last seven days are no exception.

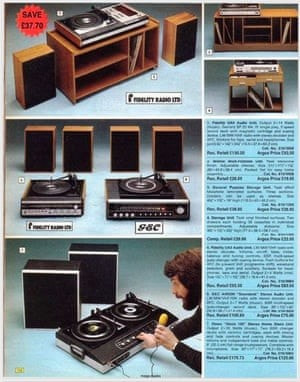

Clear Digital Digest: Argos catalogue RIP, retail tie-ups, Q2 updates and soccer supervillains3/8/2020  Argos catalogue from 1983 Today’s Clear Digital Digest starts with a look back at the beloved Argos catalogue before looking forward to the growing impact of another Argos innovation in Click & Collect, as well as other retail partnerships. Then we turn our attentions Stateside to review Q2 updates from Amazon, Facebook and Google plus the latest digital innovation in sports watching… END OF AN ERA – GOODBYE ARGOS CATALOGUE So RIP the Argos catalogue – as one wag noted, much easier to say than to actually do. As was widely reported on Thursday, Argos have stopped producing their twice yearly catalogue, meaning that January’s Spring/Summer 2020 edition will be its final print version. Argos now say that online shopping offers “greater convenience” than flicking through a catalogue, part of the continuing wider shift to ecommerce sales. Having previously spent 8 years in various roles within Argos’ ecommerce operation, during which time the catalogue’s ubiquity (estimated to have been in approx. 75% of British homes at one time) certainly helped to mutually drive web sales, there’s definitely a sense of nostalgic regret to see the “laminated book of dreams” bid farewell.  The Argos Spring/Summer 2020 catalogue However, it appears that less and less were being printed, with 3.9m of the last edition down from a peak of over 10m a decade ago. And with each catalogue costing roughly £3 to produce back when I was working there, changing shopping habits will have made ceasing production an increasingly attractive option for the huge potential cost savings; something that has been frequently reviewed over the years. Nostalgia for kids being able to choose their favoured Christmas presents will be partly assuaged by the news that Argos plans to continue to print its Christmas Gift Guide, still generally a sturdy 300 pages or so, albeit well down on the 1800 page behemoth that was the main catalogue. Before then, for anyone after a quick nostalgic fix, the Guardian pulled together a selection of vintage covers and catalogue pages, count me in for 1976’s Home Stereo Disco Unit (item 7 below…)  Argos Catalogue, 1976 CLICK AND COLLECT/RETAIL PARTNERSHIPS Of course, there are other retail channels that Argos pioneered which remain highly relevant and continue to grow in popularity, none more so than Click & Collect. In line with all ecommerce sales, Click & Collect orders have been growing rapidly since the start of lockdown, with more and more brands partnering together for mutual benefit. Argos have offered a collection service for selected eBay customers since 2014, while the introduction of Argos collection points into many Sainsburys stores since being bought by the grocer in 2016 meant that Argos was able to continue offering C&C services throughout lockdown.  Amazon entered into a similar partnership with Next last year with their Amazon Counter initiative, while John Lewis have recently announced plans to extend their C&C tie-up with the Co-op to over 500 stores. John Lewis have also just stated that they expect 60% of their sales to be online, up from 40% pre-Covid. In an update to all John Lewis partners, chair Sharon White said “We have two of the best loved and trusted brands in the UK, rated highly for our personal service and expert, impartial advice. Customers are, however, shopping in very different ways – younger people especially – with the pandemic accelerating the importance of digital. We expect John Lewis to be a 60% online retailer, from 40% pre-Covid-19, and Waitrose to rise above 20%, from 5%.” Such uncertain times do certainly seem to be leading to a much wider array of complementary brands working together, with another recent example seeing Sainsburys starting to provide a range of 3000 products to the garden centre retailer Dobbies. Q2 UPDATES: AMAZON, FACEBOOK, GOOGLE Three of the tech giants have provided their latest global Q2 updates in the last few days, with varying results. Of course, Q2 2020 is the first quarter since the world has been in lockdown, so one would certainly not expect standard trends from these updates.

AND FINALLY… In a week when it was announced at the last minute that planned pilot sporting events were not allowed to admit limited spectators as originally planned, technology continues to serve up increasingly sinister options instead. After previously highlighting Japanese robotic baseball fans last month, MLS in the US have now seemingly opened applications for the world’s next supervillain…  |

Jim ClearLead blogger and founder of Clear Digital: talking about ecommerce, digital, marketing and media.

Categories

All

Archives

December 2020

|