Today’s Clear Digital Digest reviews a recent survey on changing customer attitudes as well as the latest IPA Bellwether marketing spend report. The MP3 is 25 years old this week and although not widely used these days, as the key tech that paved the way for streaming its influence can often be understated, as we explore below. Plus a look across the Channel at a new, unique way to watch films… CONSUMER ATTITUDES AND MARKETING SPEND Amongst the latest insights that emerged this week, Wunderman Thompson’s “Covid, Commerce and the Consumer” report stood out, based on a survey of 2000 UK consumers in early June. Some key highlights include:

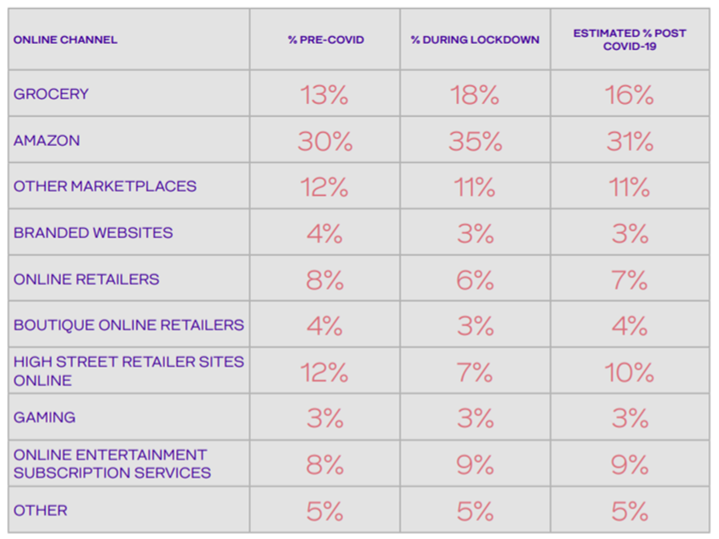

Estimated lockdown % online shopping share, source: Wunderman Thompson

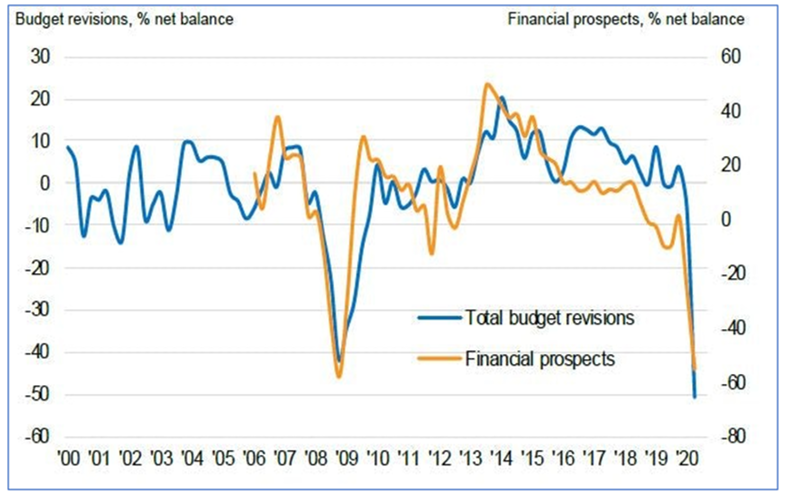

IPA Bellwether Report, source: IPA/Marketing Week MP3 TURNS 25 There was an important but fairly unheralded digital milestone this week, as the MP3 file turned 25.

AND FINALLY... With cinemas closed until recently and only gradually re-opening now, one new trend has been the emergence of drive-in cinemas to bring some US retro flavour to cinephiles who are seeking more than another Netflix binge. Venues as varied as Brent Cross Shopping Centre car park and Alexandra Palace will be accommodating such yearnings this summer. However, Haagen-Dazs are adding a new flavour in Paris with their “Cinema Sur L’Eau” concept: a socially distanced cinema where customers will sit in boats rather than cars. Further investigation reveals they will be showing a film entitled Le Grand Bain (English title: Sink Or Swim), about a group of men who start their own synchronised swimming team. Certainly a wiser choice of movie to show in this environment than Jaws or Titanic.

0 Comments

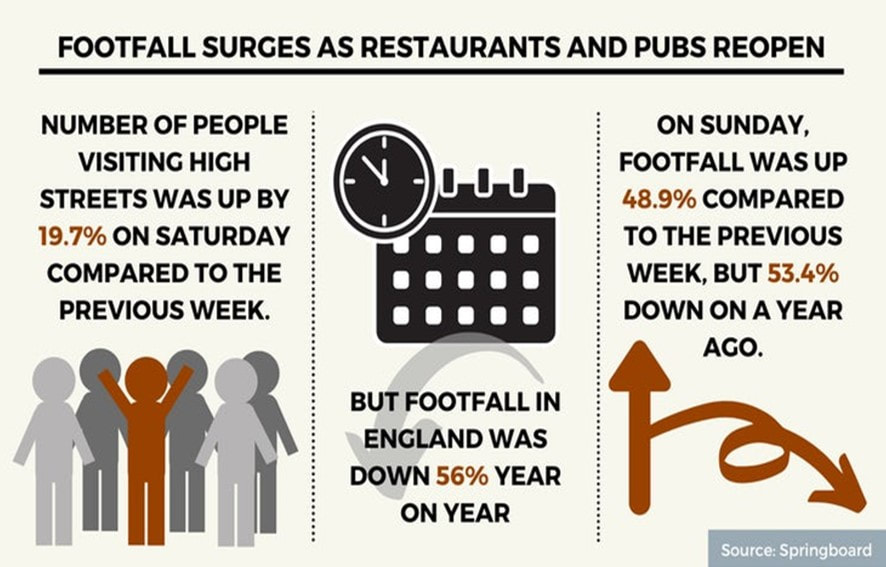

Today’s Clear Digital Digest looks at the early impact of the lockdown slightly easing last week, some updated ecommerce sales trends, Ofcom’s research regarding online usage habits and perceptions plus perhaps the scariest sports supporters seen for many a year. HAIRCUTS BEFORE HEINEKEN One of the biggest changes in the UK in the last week has obviously been the lockdown easing last Saturday (4th July) for both pubs and restaurants as well as for some other service retailers, most notably hairdressers.

ECOMMERCE SALES UPDATES

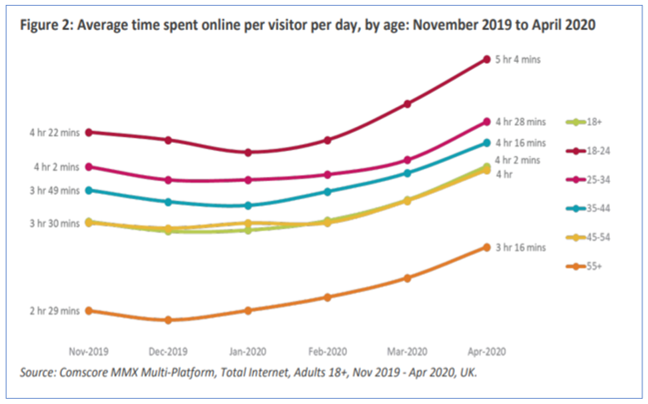

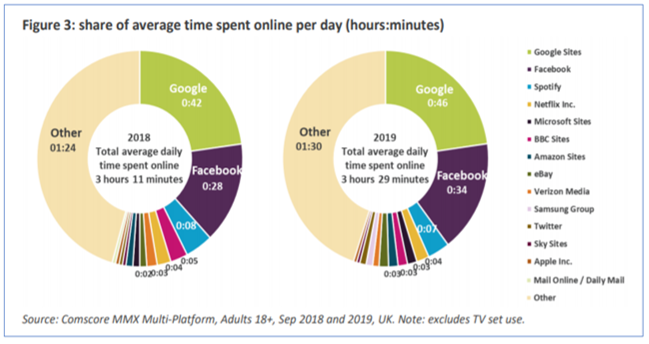

ONLINE NATION Ofcom last week released their latest report “Online Nation” that looks at what people are doing online as well as their attitudes to and experiences of using the internet.

AND FINALLY… In the week that cricket was the latest sport to return behind closed doors, its sporting cousin baseball showed off an imaginative replacement for supporters in the stadium. Japanese baseball team Fukuoka SoftBank Hawks unleashed 2 different types of robotic fans for their match against Rakuten Eagles on Tuesday, who arguably look scarier than Millwall fans from the 1980s…  Discogs is a digital brand with a difference – it’s thriving in the hugely competitive music sector, not by taking on streaming behemoths such as Spotify or Apple, but instead by catering to the niche but dedicated sector of music enthusiasts and record collectors that value the tactile and artistic value of the traditional LP or CD. From its origins as a community based purely around electronic music, Discogs has steadily evolved to encompass all genres. As well as serving as an IMDB meets Wikipedia resource for music fans, Discogs’ increasingly popular Marketplace allows collectors to buy and sell online, with nearly 15m records traded in 2019, up 34% on the year before. So far in 2020, usage of Discogs has rocketed still further, as we have all needed to focus on home-based leisure activities plus the temporary closures of all record stores. Having previously taken a detailed look at the “vinyl revival” in late 2015 when I focused on the “record shop renaissance” and how these establishments were diversifying in order to survive and thrive, I thought I’d take another look at the music sector, but this time with the specific focus on a recently growing niche digital specialist, i.e. Discogs. Therefore, this blog reviews the current music market as a whole, before delving deeper into the second hand vinyl market, a much under-researched area. Discogs’ offering is then examined, reviewing how Discogs’ recent success has been achieved as well as a typical Discogs customer journey.

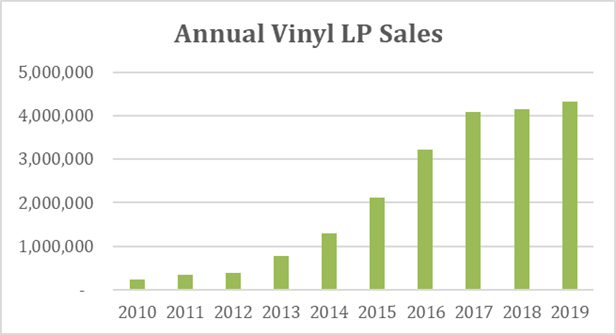

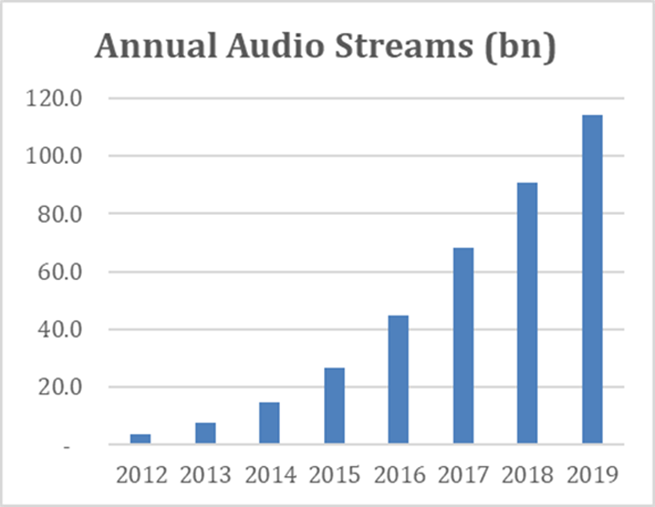

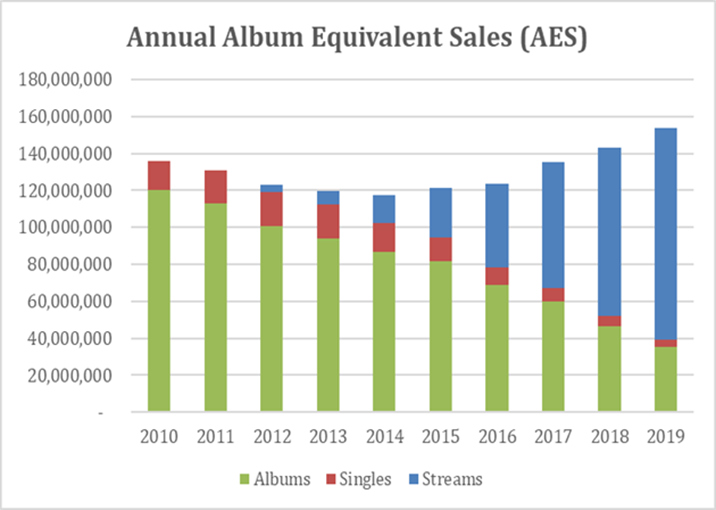

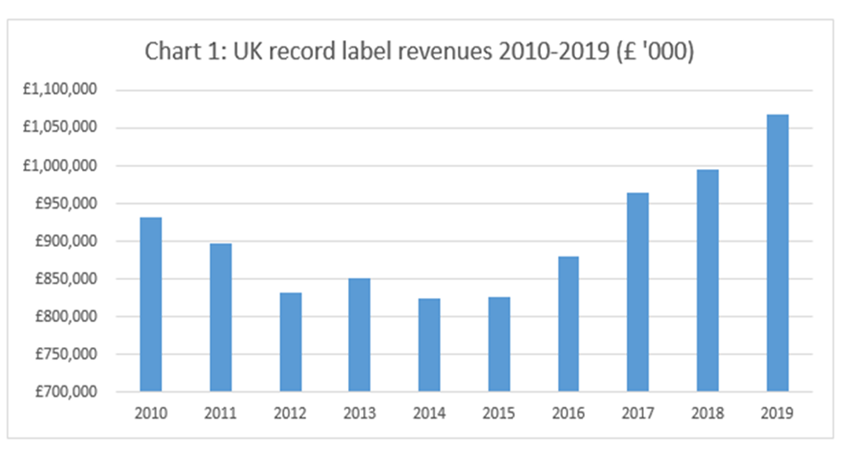

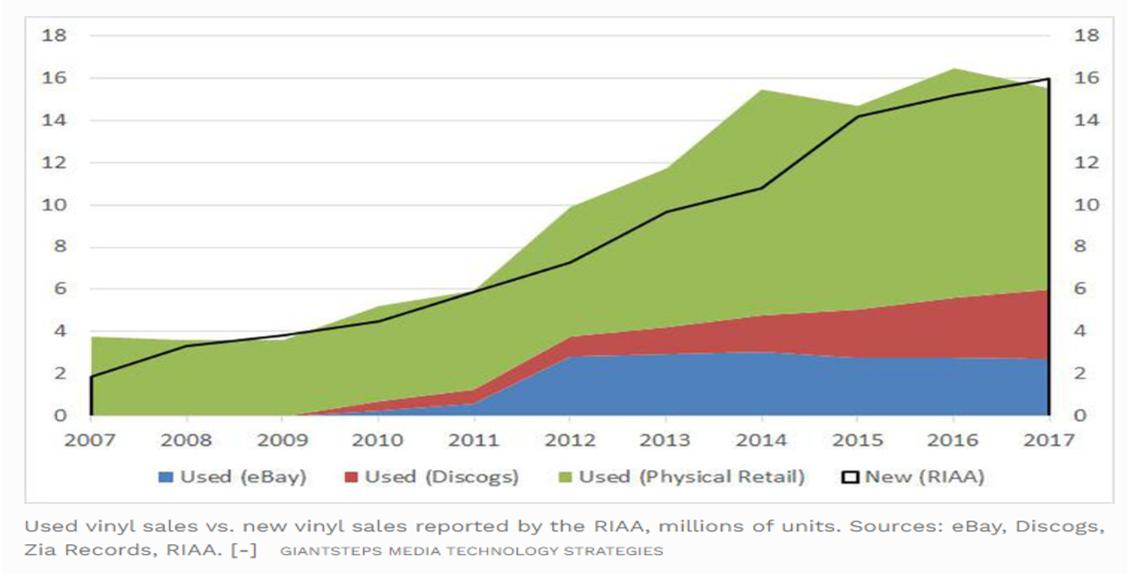

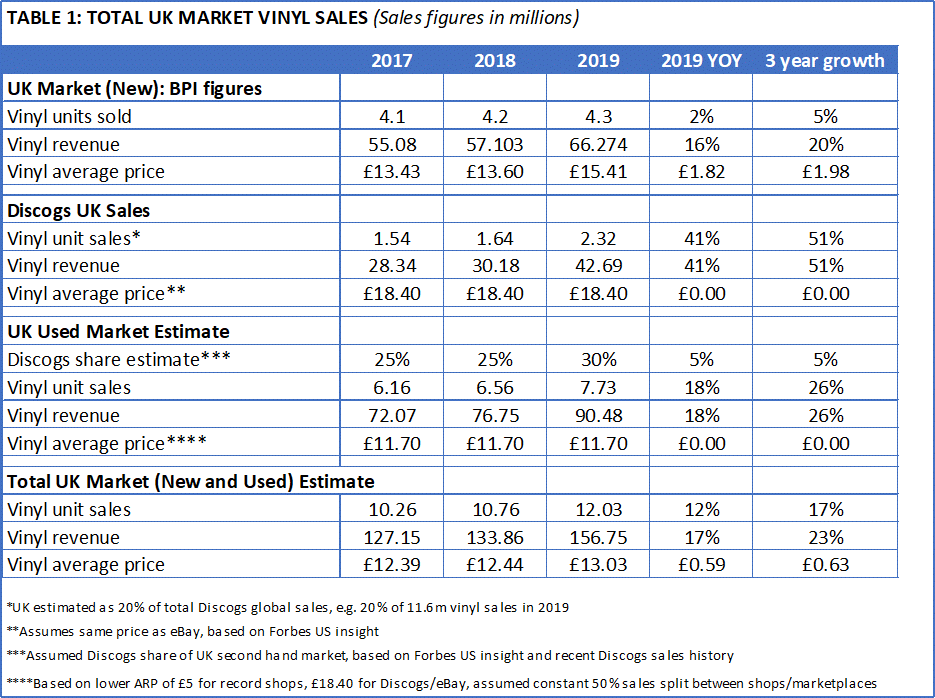

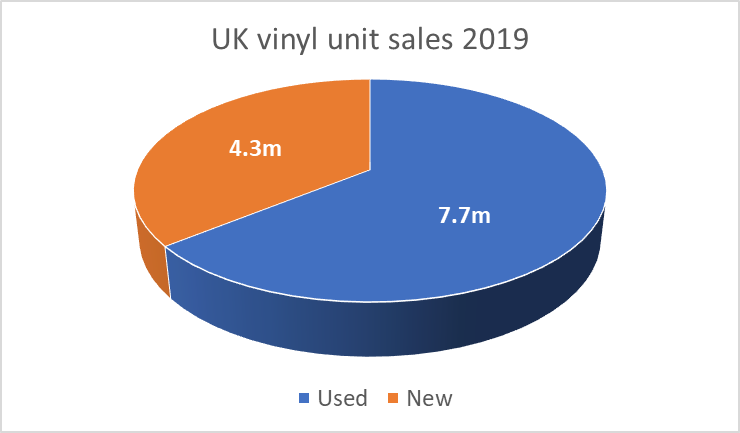

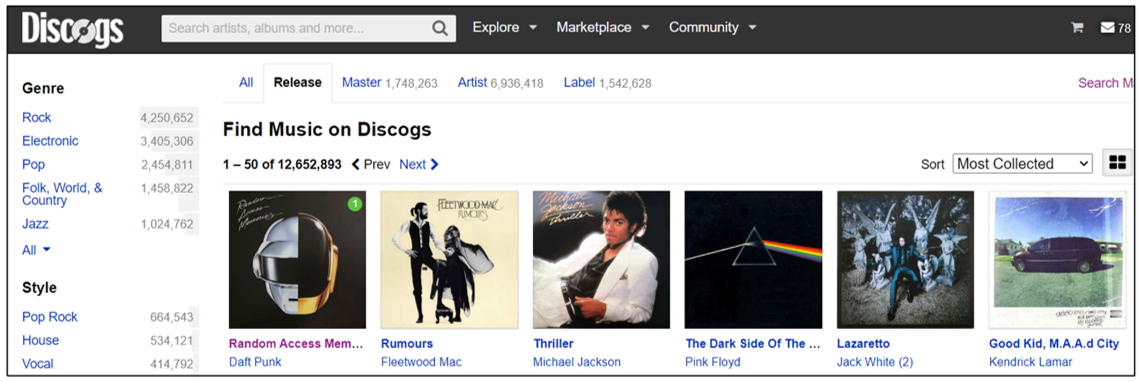

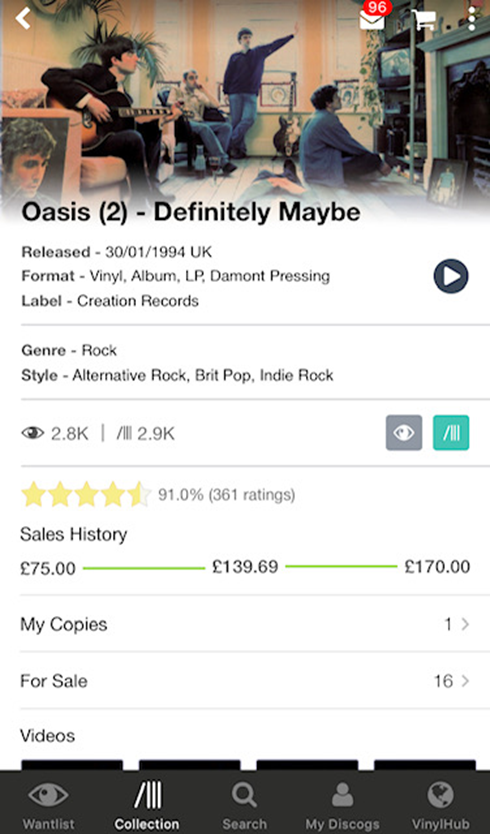

THE UK MUSIC MARKET When Clear Digital last reviewed the music market, we quoted BPI figures that vinyl sales were up 56% in the first half of 2015 and on track to hit 2m records sold for the year, which would be the highest figure since the early 1990s; although still a small fraction of the 80m routinely sold during the late 1970s. Vinyl sales did indeed exceed 2m in 2015, with sales of 2.1m and have continued to rise since then, more than doubling in the subsequent 5 years to reach 4.3m in 2019; albeit growth has slowed considerably during the last 3 years as the graph below demonstrates:  Source: BPI The big news in the music industry over the last 5 years has of course been the rise of streaming services, spearheaded by Spotify with Apple Music, Amazon Music, Deezer et al. Streaming in the UK passed a significant milestone last year, with over 100bn tracks streamed for the first time, a total of 114bn, up 26% on 2018’s 91bn.  Source: BPI The dominance of streaming this decade has seen the music industry create a new metric in order to compare distinct formats: the Album Equivalent Sale (AES). AES equates 100 streams as equivalent to purchasing one single “track” and 10 “tracks” as equivalent to an album, thus meaning that 1000 individual songs streamed is viewed as equivalent to one physical album purchased.  Source: BPI As the graph above shows, 2019 was a strong year for music consumption, with 153.5m annual AES, +7.5% on the prior year and the highest of the decade. Streaming drove this increase, with 114.2m AES streams (+26% YOY), while 28m physical albums were sold (-23% YOY). These 28m include the 4.3m vinyl LPs (+4% YOY) mentioned earlier as well as 23.5m CDs, a format which continues to rapidly decline, with annual sales down 26.5% YOY. And having found a way to generate revenue from streaming services, record label revenues have also increased steeply in recent years, from a low of £825m in 2014 to £1.07bn in 2019, the highest such figure since £1.17bn was recorded in 2006.  Source: BPI Streaming income of £629m accounted for 59% of total record label revenue in 2019 – with subscription revenue by far the most significant chunk generating £568m, with ad-supported streaming revenue contributing £25m and video streaming providing £35m. Physical sales of £216m made up just 20% of industry revenue, with CD sales of £142m down 20% YOY. However, vinyl revenue of £66m grew by 16% YOY, despite unit sales of 4.3m growing by just 4% YOY. CD revenue of £142m declined by 20%, meaning that while still the dominant traditional format, vinyl is taking an ever larger proportion of the amount spent on physical music. However, the total amount that consumers actually spend on physical records (and especially LPs) is grossly under-reported by industry bodies and most media as Bill Rosenblatt states in an excellent Forbes article: “Vinyl is bigger than we thought. Much bigger”. THE SECOND-HAND/USED VINYL MARKET Bill Rosenblatt mentions the vinyl revival of the last decade, but also highlights that “vinyl sales are actually much larger than what industry figures report, because they don't count used vinyl sales and they under-count new vinyl sales. Now, thanks to some new data, we know that the true size of the vinyl market is more than double those industry figures”. As revenue from second-hand records does not go to record labels or artists, the industry does not count them, prompting Ron Rich, SVP of Discogs Marketplace to say “Given the size of the overall market, I am always shocked that these numbers are ignored when reporting sales”. It is indeed challenging to obtain data on second-hand sales, but Forbes managed to secure sales figures from the two leading online players, namely eBay and Discogs, as well as work with a chain of independent record stores to calculate overall store sales.  Source: Forbes As the graph above demonstrates, second-hand unit sales in 2017 matched the 16m vinyl records reported by the RIAA, the US equivalent of the BPI. And this figure would increase further had Amazon (the third biggest player in online second-hand records) provided data for the used records comparison. Discogs’ recently published “State Of Discogs 2019” report states that Discogs sold 14.6m items globally in 2019, 34% on the prior year. Vinyl accounts for an ever growing lion’s share of Discogs’ sales, with vinyl sales of 11.6m units, +41% YOY. Breaking this down into the UK, we can estimate that Discogs sold 2.3m vinyl records in the UK last year, creating total sales revenue of £42.7m (with £3.4m commission for Discogs, at their 8% rate). In total, it is estimated that some 7.7m vinyl records were sold second-hand last year, 80% higher than the volume of new records quoted by BPI (4.3m). Further validation on volume is provided by eBay stating that they sold 4 vinyl records per minute in 2017, equating to 2.1m units in total and a 34% market share that year.  These 7.7m records generated an estimated used revenue of £90.5m, well above the £66.3m spent on new vinyl. This leads to total vinyl sales revenue of £157m, of which only 42% is generated by the new music industry and directly reported on. This split reflects the US market as previously outlined by Bill Rosenblatt at Forbes: “thanks to some new data, we know that the true size of the vinyl market is more than double those industry figures”. Total physical new and used records (i.e. CDs plus vinyl) together generated sales of £302m in 2019, an extra £94m above the combined BPI reported figure of £208m, with £91m of this accounted for by second-hand vinyl. In 2019, 64% of vinyl records purchased were second-hand (7.7m, 58% of total spend) meaning that the widely reported figure of 4.3m vinyl LPs sold last year is severely under-stated; the true figure is more in the region of 12m.  REVIEWING DISCOGS’ RECENT SUCCESS A potent mixture of Wikipedia, IMDB, eBay and Pokemon for music fans, Discogs was originally established in 2000 by Kevin Lewandoski purely to catalogue dance records but now describes itself as “the world's foremost Database, Marketplace, and Community for music”. From an initial 2200 users in its first year, Discogs now has over 7m active users and a database of over 12.6m releases listed. Originally focused purely on electronic records, Discogs gradually increased its remit, with rock releases becoming the dominant genre in 2016. Adding to the collection can be theurapetic and also addictive, but it was the launch of the Discogs marketplace in late 2005 that really planted the seed for Discogs’ future success.  The cornerstone of Discogs is its Collection feature that allows users to easily create their own online record collection, from the 12.6m existing releases in the Discogs database. Users can opt to search via the Discogs website or app, which has a built-in barcode scanner, making this a much simpler process to locate your particular record (for those that have barcordes anyway!). Similar to Wikipedia, Discogs is reliant on its users to add new releases, as well as providing further information (e.g. extra pictures, song videos etc). 11.6M records were added to their collection in April 2020 by 306K users, well up on the more recent annual average of 7M per month due to lockdown. By way of comparison, the average submission in 2014 was just 2M per month. This collection spurt is also helped by the addictive/gamified nature of adding records, as you are able to get an updated total of how much your collection is worth based on recent sales in the Discogs Marketplace. Discogs will look at the most recent 10 sales of the relevant release and show its lowest, median and highest selling price. This then feeds up to your personal collection homepage with a min/med/max estimated value, thus encouraging the user to add as many records as possible to see this figure increase and increase…  "Definitely Maybe" original pressing listed on the Discogs App, recently sold for between £75 to £170, with a median selling price of £139.69 The Discogs Marketplace was launched in late 2005, due to user demand – as CEO Kevin Lewandoski has stated: “The users asked for it. There was already a "collection" and "want list" feature, and a lot of people asked for a "sell" list, just to have a list of things that they were selling…Amazon and eBay were around, but they weren't really what they are today.” There are over 50M records available globally on the Marketplace, with 9M from sellers in the UK. Sellers vary from individuals selling off unwanted/spare items from their collection to sole traders to established second-hand record shops. As outlined in the music industry section, the Discogs Marketplace has become an increasingly prominent player in the second-hand market, selling 14.5m records in 2019. Of these, 11.6m were vinyl, which increased sales by 41% on 2018. DISCOGS – CLOSING THOUGHTS Discogs has recently experienced strong growth, both commercially (with Marketplace sales +34% in 2019) and general usage, with 11.6m records added to users’ collections in the first month of lockdown, 65% above the usual monthly average of 7m. And despite the marketplace sector being dominated by Amazon and eBay, with 90% share between them (as the complementary “The UK Marketplace Sector – And The Role Of Community” Clear Digital research explores), Discogs managed to grow sales faster than either in 2019. 3 key dynamics helping to drive Discogs’ success are:

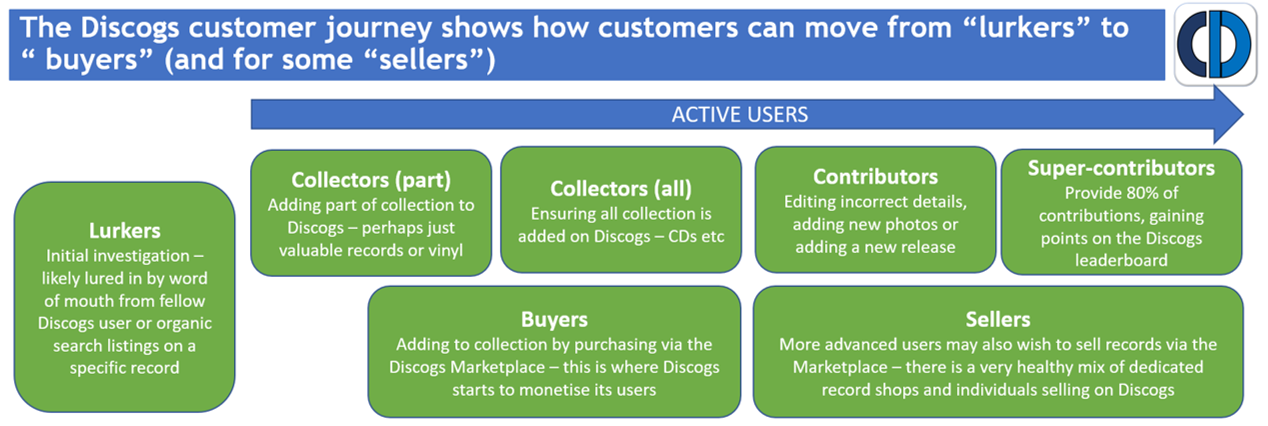

Breaking down the Discogs customer journey as shown below, we can see how customers move from “lurkers” to the more profitable “buyers”, and in some cases “sellers”, all underpinned by the strong Discogs community of half a million contributors, essential to the richness of its experience…  Please note that this blog is a summary of the accompanying deeper dive on “Discogs: the digital success story of the vinyl revival” which is available to download here

It’s now just 3 weeks to go till Euro 2016 kicks off in France on Friday 10th June, and while the tournament itself will have some way to go in order to match the still incredible story of Leicester City’s domestic Premier League triumph, the extra home nation interest this year will undoubtedly see passion levels run high once Euro 2016 actually starts. Summer football events such as the Euros are now also an established part of the marketing and promotion calendar for many brands – for both official sponsors and other companies – so I’ve taken a look at how some of them have so far embraced this opportunity. It was estimated that the 2014 World Cup contributed £2.5bn to UK consumer spending and it is believed that Euro 2016 will generate a similar amount, with food, drink, retail and betting sectors seeing the greatest benefits. Over 60% of pubs are predicting like for like sales increases of more than 10% through June, with the England v Wales group match on Thursday 16th June unsurprisingly highlighted as a particularly large opportunity.  Pubs are expecting a significant sales uplift during Euro 2016. Source: Morning Advertiser/MatchPint The nature of big sporting tournaments like Euro 2016 lends itself to a variety of different objectives for brands, in particular:

OFFICIAL SPONSORS: CARLSBERG EARLY PACE-SETTERS UEFA have 10 official sponsors for Euro 2016; ranging from the usual suspects such as Adidas, Coca-Cola and McDonalds to emerging brands which won’t be as familiar to European consumers. These include the Chinese consumer electronics company Hisense and the seemingly aptly named Socar. Socar is actually the State Oil Company of the Azerbaijan Republic, so in reality this organisation is perhaps not such a natural fit for football tie-ins as Carlsberg for example.  Amongst official sponsors, Carlsberg have certainly been to the fore with their activation plans, with a range of initiatives all following the “if Carlsberg did…” strapline, seemingly both in domestic markets and pan European too. This week, Carlsberg have been trailing online a new ad campaign starring Marcel Desailly, one of France’s World Cup 98 and Euro 2000 winning heroes. “If Carlsberg Did La Revolution” will undoubtedly feature heavily in June during TV coverage, with many hidden references in there for football geeks as well. Amongst the standard ticket giveaway competitions, Carlsberg have also been using more creative methods ahead of the tournament in the UK, including Chris Kamara looking at what would happen “if Carlsberg did substitutions” and rewarding generous Tube travellers with tickets to the Euros. Other UK focused campaigns include experiential activity, with Carlsberg rebranding 19 English pubs as the patriotic “The Three Lions”. Some other selected highlights from official sponsors include:

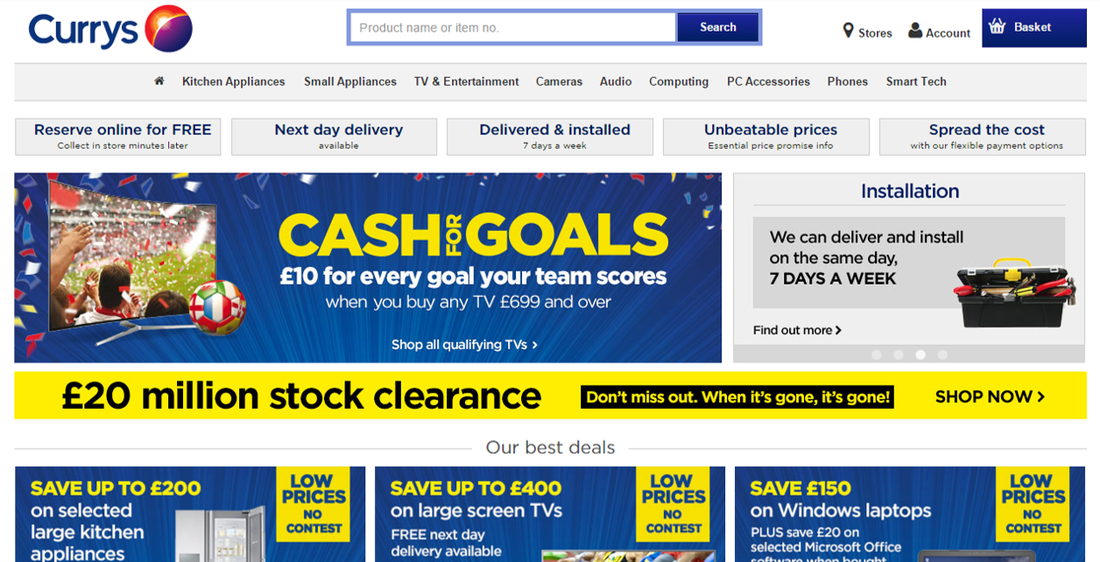

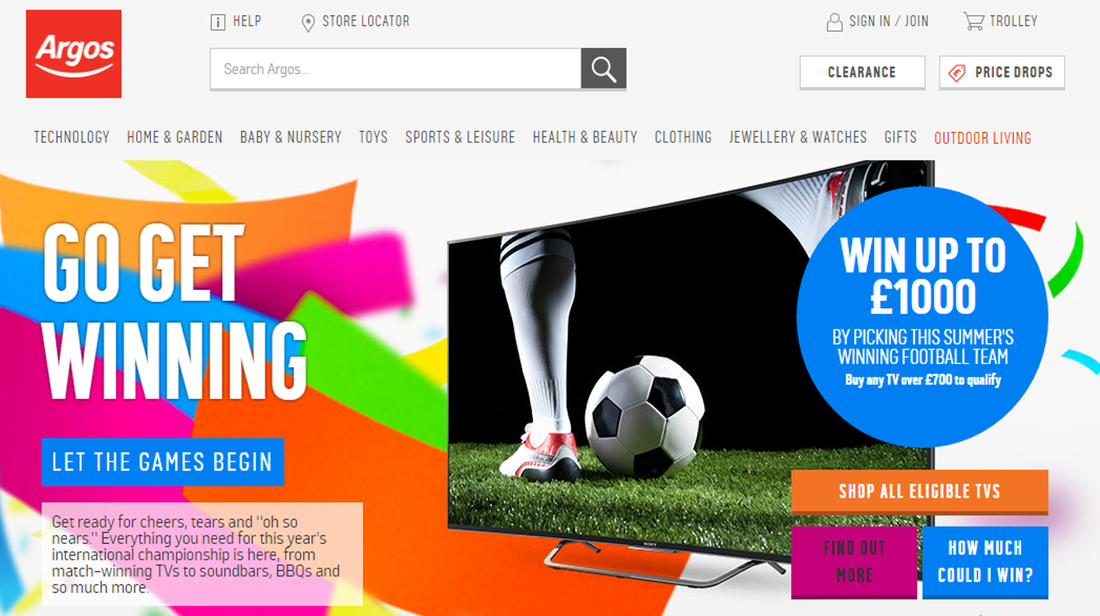

“UNOFFICIAL” CAMPAIGNS: PREDICT THE WINNER 3 weeks out and it may be a bit early to stock up on essentials like food and drink if planning a barbecue party, but it is the perfect time for more considered purchases to enhance your Euro 2016 viewing pleasure, such as a shiny new TV. And full disclosure here: I did once buy a new TV in time for Euro 2004, so this does actually happen! However, with governing bodies such as UEFA monitoring and protecting their trademark rights to enhance the aforementioned sponsorship deals, this tends to result in some creative descriptions by the vast majority of brands that are not filling UEFA’s coffers; leading to the use of many generic campaign titles such as the “summer of sport" rather than the trademarked "Euro 2016" or similar. A couple of good examples here are provided by Currys and Argos, both of whom are offering TV promotions with a prediction element based around "this summer’s big football tournament" (aka Euro 2016).  To the fore on Currys’ homepage is their “Cash for Goals” promotion, backed up by a range of accompanying media both online and offline. This is a deal that Currys have run in similar form during previous summer football tournaments, and means that should you spend over £699 on a TV, Currys are offering £10 cashback for each goal that either England, Wales, Northern Ireland or Republic of Ireland score during the tournament. Customers can pick their team and with more choice amongst British Isles teams than usual, it will certainly be interesting to see if customers patriotically pick their own home nation, or go for another team based on their perceived chances.  Argos are also focusing on upper end TVs by offering customers a chance to win up to £1000 by “picking this summer’s winning football team” when you buy a TV over £700 in their “Go Get Winning” promotion. Further investigation shows that for those heartened by the Leicester fairytale, you can win £1000 back if you plump for an outsider like Albania or Slovakia (or Northern Ireland/Wales), down to £100 for France, Germany or Spain. An England win, unlikely as it may seem, would net you £250 cashback. AND FINALLY… As well as official Euro 2016 sponsors maximising their activity with glossy campaigns and giveaways, plus retailers looking to sell appropriate seasonal products, multi-national sporting events generally also see a few more esoteric tie-ins as well. Expect to see some of these to the fore as the tournament approaches, but as a tasty example, the Amazon listing below provides some food for thought…  What's the most popular British TV programme? And what other big event is on the horizon? These Euro 2016 cake toppers provide an ideal baking/football mash-up This week saw Ofcom release their always useful and insightful annual UK media review: Adults Media Use and Attributes 2016. At over 200 pages, there is a huge wealth of detail to take in at once, but this report can prove an invaluable one stop shop over the year for many must have stats. A good place to start is the report overview which pulls out 4 major trends, with the ever moving shift to smartphone usage unsurprisingly to the fore:

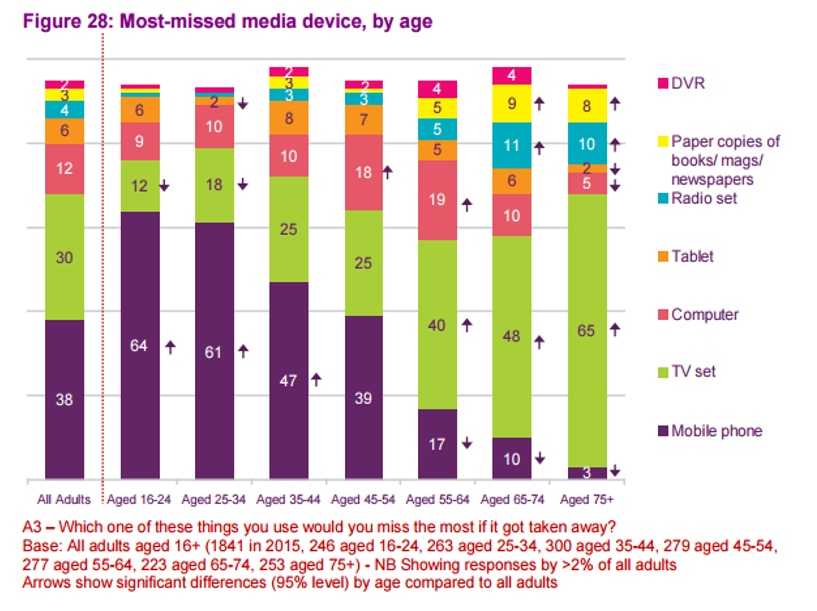

Mobile phones would now be more missed than TV by all age groups up to 55. Source: Ofcom I spent yesterday at the Internet Retailing Expo and these trends around shifting device usage were resonating loud and clear from some of my discussions there plus presentations attended; I’ll be blogging more thoughts on this next week. Returning to the Ofcom report, I’d recommend a couple of other interesting summaries:

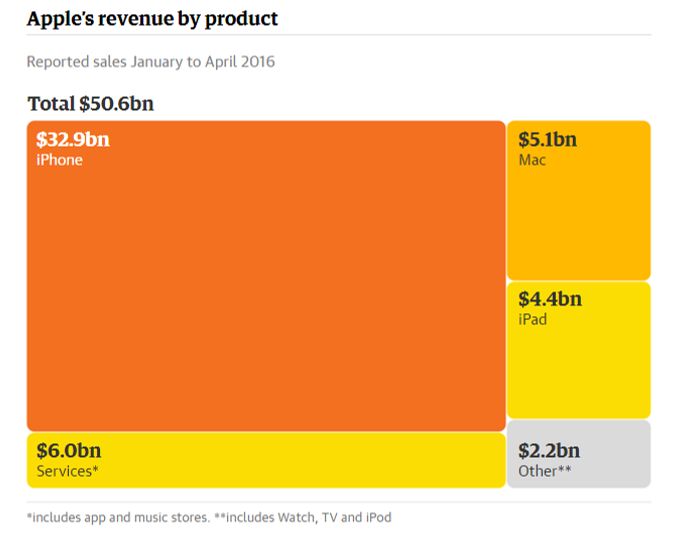

Some diverging results statements from the internet’s big beasts this week. Although widely trailed before, it was still strangely odd to see Apple report its first fall in sales since 2003 on Tuesday, with sales of quarterly sales of $50.6bn down from $58bn in the same quarter last year. This was primarily due to a slowdown in iPhone sales (which account for 65% of Apple’s revenue) to 51.2m in the quarter from 61.2m the year before. This of course led to a wealth of think pieces on what Apple needs to do to turn this decline around (spoiler alert: it is unlikely to be the Apple Watch), while I did enjoy this “brief guide to everything that’s annoying about Apple” – my personal favourites being numbers 5 and 11.  iPhone revenue dwarfs all other Apple divisions. Image source: The Guardian Meanwhile, Amazon has just posted its fourth straight profitable quarter in a row, and the largest quarterly profit in its history, prompting Wired to exclaim “Whoa, Amazon Isn’t Just Making Money. It’s Making More Than Ever”. Amazon’s Q1 net profit stood at $513m with global revenue of $29.1bn, up 28% on last year and beating analysts’ expectations, leading to a share price increase of over 12%. It’s worth stating here that Amazon spent years incurring losses as it built its huge empire (including its increasingly important AWS cloud computing arm which saw revenue up 64% YOY to $2.6bn), but has now posted ever growing profit growth for the 4 quarters of the last year; a development sure to please investors but also demonstrating that Amazon seems to be entering its next phase of maturity.

|

Jim ClearLead blogger and founder of Clear Digital: talking about ecommerce, digital, marketing and media.

Categories

All

Archives

December 2020

|

||||||