Today’s Clear Digital Digest reviews a recent survey on changing customer attitudes as well as the latest IPA Bellwether marketing spend report. The MP3 is 25 years old this week and although not widely used these days, as the key tech that paved the way for streaming its influence can often be understated, as we explore below. Plus a look across the Channel at a new, unique way to watch films… CONSUMER ATTITUDES AND MARKETING SPEND Amongst the latest insights that emerged this week, Wunderman Thompson’s “Covid, Commerce and the Consumer” report stood out, based on a survey of 2000 UK consumers in early June. Some key highlights include:

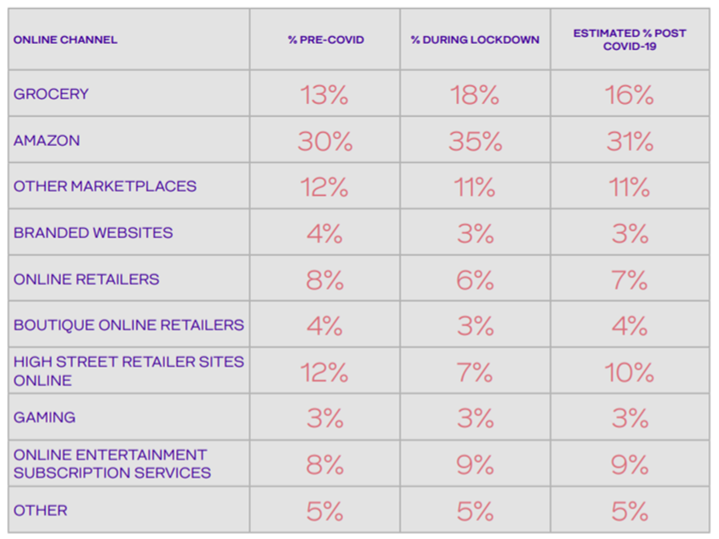

Estimated lockdown % online shopping share, source: Wunderman Thompson

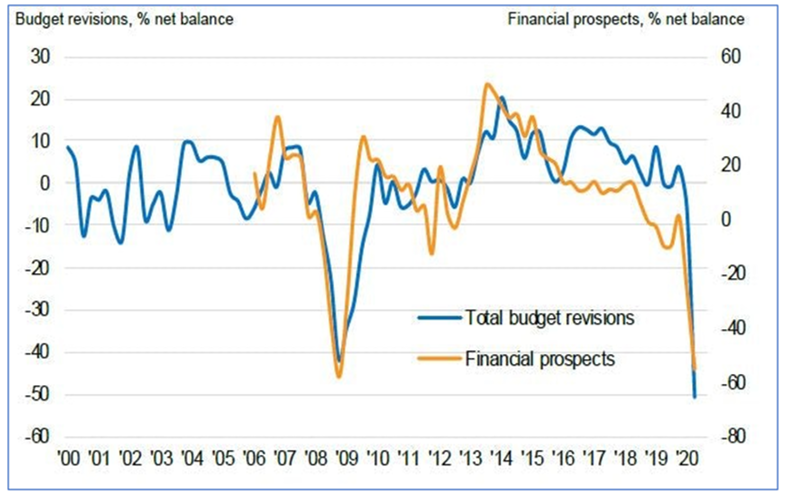

IPA Bellwether Report, source: IPA/Marketing Week MP3 TURNS 25 There was an important but fairly unheralded digital milestone this week, as the MP3 file turned 25.

AND FINALLY... With cinemas closed until recently and only gradually re-opening now, one new trend has been the emergence of drive-in cinemas to bring some US retro flavour to cinephiles who are seeking more than another Netflix binge. Venues as varied as Brent Cross Shopping Centre car park and Alexandra Palace will be accommodating such yearnings this summer. However, Haagen-Dazs are adding a new flavour in Paris with their “Cinema Sur L’Eau” concept: a socially distanced cinema where customers will sit in boats rather than cars. Further investigation reveals they will be showing a film entitled Le Grand Bain (English title: Sink Or Swim), about a group of men who start their own synchronised swimming team. Certainly a wiser choice of movie to show in this environment than Jaws or Titanic.

0 Comments

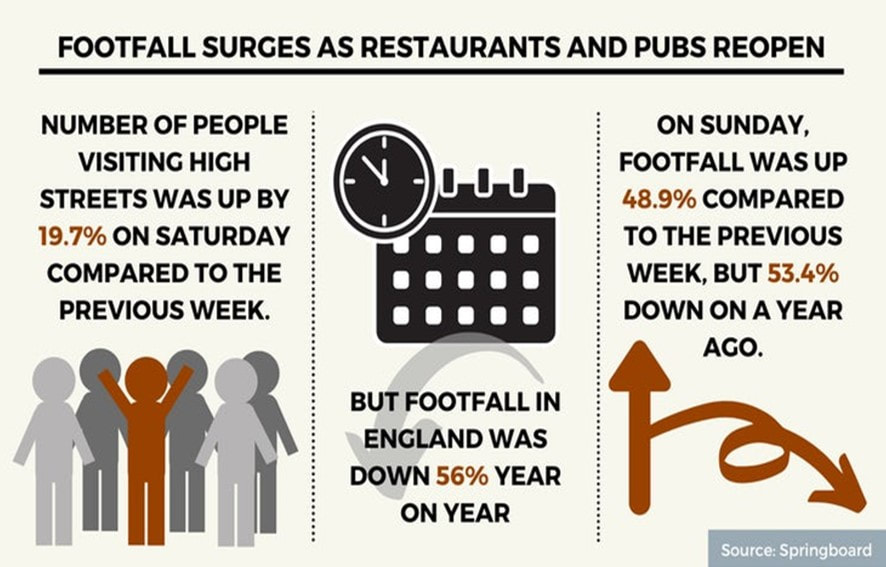

Today’s Clear Digital Digest looks at the early impact of the lockdown slightly easing last week, some updated ecommerce sales trends, Ofcom’s research regarding online usage habits and perceptions plus perhaps the scariest sports supporters seen for many a year. HAIRCUTS BEFORE HEINEKEN One of the biggest changes in the UK in the last week has obviously been the lockdown easing last Saturday (4th July) for both pubs and restaurants as well as for some other service retailers, most notably hairdressers.

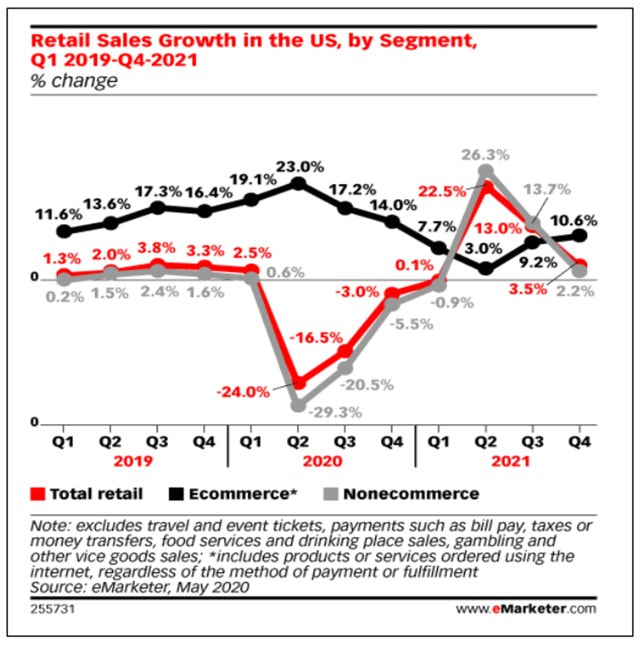

ECOMMERCE SALES UPDATES

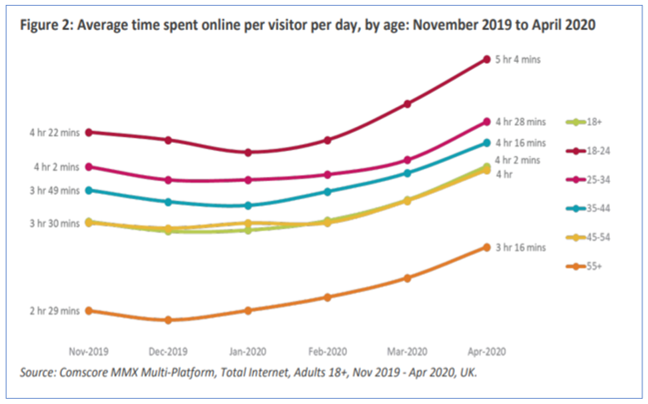

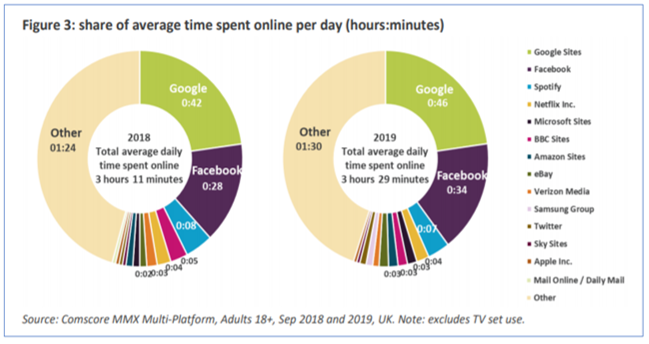

ONLINE NATION Ofcom last week released their latest report “Online Nation” that looks at what people are doing online as well as their attitudes to and experiences of using the internet.

AND FINALLY… In the week that cricket was the latest sport to return behind closed doors, its sporting cousin baseball showed off an imaginative replacement for supporters in the stadium. Japanese baseball team Fukuoka SoftBank Hawks unleashed 2 different types of robotic fans for their match against Rakuten Eagles on Tuesday, who arguably look scarier than Millwall fans from the 1980s… Hi and welcome to the first Clear Digital Digest for a while, as the Clear Digital blog returns. More about that here but as before, these summaries will select a range of recent interesting, insightful and sometimes quirky ecommerce, marketing and media stories and break them down into handily digestible form. Today we’re looking at some new research on the world’s largest brands, the increasingly polarised nature of the UK retail market plus a novel way to socially distance ahead of lockdown restrictions further easing this weekend… AMAZON REMAINS THE WORLD’S MOST VALUABLE BRAND, BUT FACEBOOK FALLS

Source: Kantar/Marketing Week Methodology: Kantar’s BrandZ valuation process takes the financial value created by a brand in US dollars and multiplies it by brand contribution, to calculate its Brand Value: the worth in dollars that each individual brand is tangibly worth.

Source: Kantar/Marketing Week RETAIL’S CONTINUING DIVIDE It’s been another unfortunately contrasting week of winners and losers in the retail space.

AND FINALLY… As Clear Digital returns this week, I’ve just published two deeper dives as well, both examining the marketplace sector. This is an area that has actually benefitted to some degree from the present turmoil, with recent stories including Etsy doubling its sales in April and music marketplace Discogs seeing usage levels increase by 65%.

And finally, with (some) pubs set to reopen this weekend – and mixed views as to what this will bring – I did like this novel solution from across the Channel that I discovered on Twitter this week…

Last Thursday (28th April 2016), I headed to Birmingham’s NEC for this year’s Internet Retailing Expo (IRX) to catch up with some old colleagues, attend a few conference sessions and generally take the temperature of the ecommerce sector. As one may expect, many of the big themes from the day were to some degree mobile centric and this blog pulls out what I considered to be 3 key overarching trends from the day:

NB: This blog is also available as a PDF file, downloadablehere. RECENT OFCOM DATA HIGHLIGHTS HOW QUICKLY SMARTPHONES ARE GAINING ON LAPTOPS AS THE PREFERRED ONLINE SHOPPING CHANNEL An ever accelerating customer shift to smartphone usage means that now is a true time of change for selling via digital channels. This change does however mean that a lot of standard ecommerce best practice (honed ever more knowledgeably over the last 10-15 years based on desktop usage and behaviour) is now steadily becoming outdated for a majority of customer journeys. Before delving into some data and insights gleaned from IRX itself, it is worth pulling out a couple of pertinent points from Ofcom’s recently issued Adults Media Use and Attributes 2016 report. One specific section looking at online shopping really shows the pace of change, highlighting that last year, 24% of users said that the smartphone is the device they most use to shop online; a huge rise from 15% in 2014, with this growth all coming from a decline in laptop preference (falling to 37% from 50% the year before) albeit laptops still remain the most used device overall. This is not the case for all ages, with smartphones preferred by younger consumers, just edging out the laptop for those in the 16-24 and 25-34 brackets.

Source: Ofcom (April 2016)

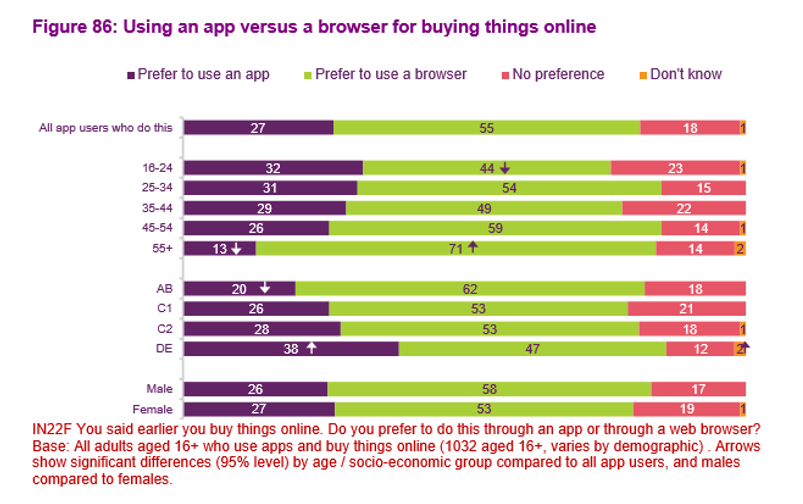

So, this helps to provide some newly updated data for an ecommerce trend that is unlikely to surprise anyone. However, something that is perhaps not so well known is customers’ preference to transact on smartphone within browsers rather than via an app, a trend that is actually fairly consistent across most age groups. With mobile app strategy a source of much discussion for retailers, with many different viewpoints and strategies, this insight seems highly valuable.

Most customers would still rather transact online with their browser than via an app. Source: Ofcom (April 2016)

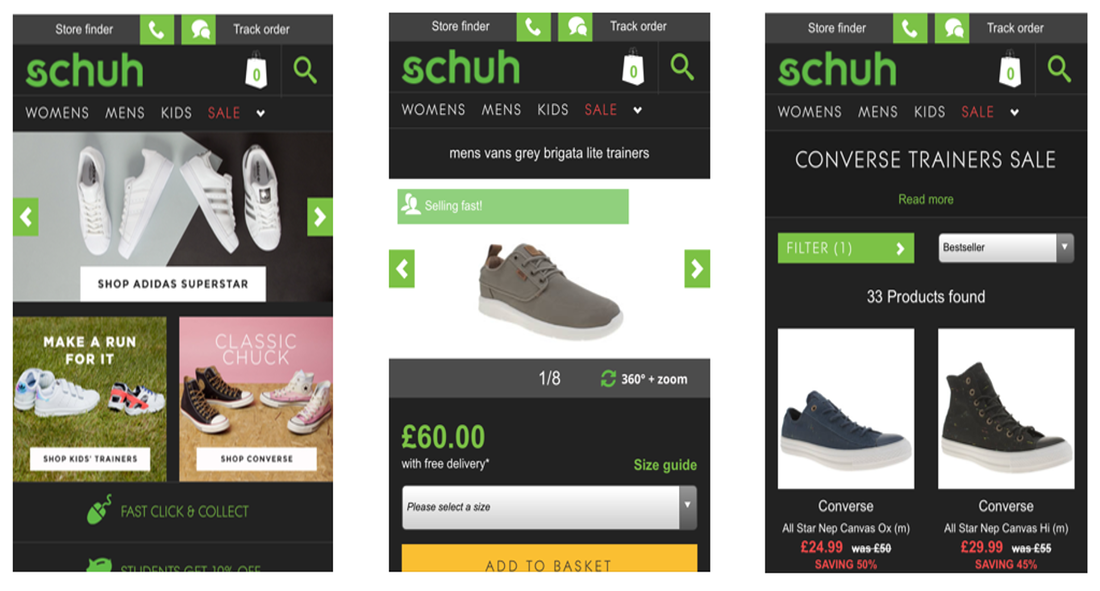

THE MOST VALUABLE IRX INSIGHTS WERE SMARTPHONE RELATED Moving on to look at IRX itself, Google’s Retail Industry Head Paul Goldstein delivered the Digital Sales & Marketing closing keynote address and as one would expect, this well attended session contained some helpful insights, principally centred on the mobile experience (and how to improve your PPC AdWords campaigns of course!). Outlining that 40% of online shoppers research on mobile but then convert on desktop/tablet may have been familiar news, but the fact that 50% of customers who conduct a local search on mobile (e.g. “buy a kettle near me”) end up in store within a day was certainly a useful statistic to demonstrate the different and unique nature of smartphone shopping. Paul’s presentation then looked into the need to “Be Personal, Be Actionable and Be Measured”; important points that I’ll return to when talking about my 3 key trends. Looking at some specific retailer examples, Schuh’s Deputy Head of Ecommerce Colin McMillan mentioned that from the 15-20% of Schuh’s overall sales that were transacted online, mobile was now accounting for nearly half its traffic (48%, compared to 30% for desktop and 22% for tablet) but a lower percentage of sales; 42% of revenue due to a reduced conversion rate of approximately 1.5% compared to the 2.5-3% seen on desktop/tablet. Some fairly common ecommerce benchmarks there, but what was intriguing was the fact that 89% of Schuh mobile shoppers only interact with Schuh digitally via mobile, so the oft voiced assumption that customers use mobile early in the buying process only to ultimately convert via desktop rather than mobile (due to factors such as ease of purchase/UX and security concerns) does not seem to apply here. Rather, Schuh has a sizeable proportion of customers for whom a smartphone is their sole ecommerce experience for the whole purchase funnel.

A likely lower than average age of Schuh shoppers would skew usage towards mobile to some degree, but this does also raise the question of why mobile conversion rate should be so much lower than for desktop if 9 out of 10 of mobile shoppers are exclusively using this as a digital channel. I believe that this seems to come down to 2 key factors: continuing difficulty with analysing all channels together (and understanding of the role each has to play) as well as ecommerce UX innovation proceeding at a slower pace than other mobile customer experiences, both of which I’ll explore more below. Before that though, it’s worth looking at the differences (and similarities) between desktop and mobile ecommerce, not least their different stages of maturity.

1. MOBILE COMMERCE IS STILL FAIRLY YOUNG, WITH ALL THE GROWING PAINS THAT IMPLIES

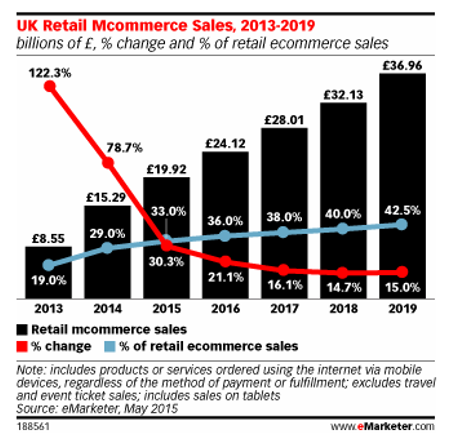

The art of designing, building and promoting standard desktop ecommerce sites is fairly well established now, with up to 20 years of practical experience, knowledge and research in this field. On the other hand, as more seasoned digital veterans will no doubt recall, despite being promised many times that the “year of mobile” was coming, it was really the iPhone’s launch in 2007 and ensuing smartphone penetration growth from the start of this decade that have led to the profound shift in consumer behaviour that has seen eMarketer forecast that UK m-commerce sales will grow nearly fourfold from £8.5bn in 2013 to a 2018 forecast of over £32bn.

So while desktop ecommerce may now have come of age and graduated, mobile commerce is about to start primary school, so it still has a lot to learn and also is likely to keep asking many hard to answer questions, for example:

Of course, the key point to remember here is that there is no “one size fits all” approach and needs will differ from company to company, even more than with desktop due to the smartphone’s nature. With recent Ofcom research highlighting that we would now miss the smartphone more than any other device – replacing the previous preferred TV and way ahead of the computer – this simply reflects that place that our mobile now takes in our life; as well as being a supremely powerful mini-computer (and of course phone!), it is also our camera, music player, GPS, torch, clock, stepometer, games console, calculator etc etc etc. Ecommerce operations will also notice this as customers use them in very distinct ways. Having heard from Schuh that mobile is their most important channel (with 48% of traffic and 42% of sales coming from smartphones), we learnt at IRX that this is very different for Eurostar, courtesy of their Head of Digital Neil Roberts. Desktop is by far their most important digital channel, accounting for 53% of research journeys and a huge 81% of purchase journeys; smartphones account for 34% of research and 9% of purchase, with tablets making up the remaining 13% of research and 10% of purchase journeys. This is likely due to various reasons – e.g. more considered and complex purchase, older demographic – but the fact that Eurostar’s mobile experience is not yet fully optimised, albeit moving to a responsive website very soon, is also surely a factor. One final IRX experience to highlight is that of MySupermarket, courtesy of UK MD Kim Ludlow. The fourth most visited supermarket site in the UK (behind only Tesco, Asda and Sainsburys), this online comparison website actually sees a majority of its customers using it to influence in-store purchases; 35% of its customers purchase online for home delivery while 65% research online and purchase offline. The mobile nature of smartphones therefore proves a strong fit with the MySupermarket experience, with 63% of shoppers using the website on their smartphone – an adoption much higher than their accompanying app which has a much lower transaction/usage rate, prompting Kim to question that if they had known how successful the site would be on mobile “would we have built it [the app]?” Therefore, Schuh, Eurostar and MySupermarket all have quite different mobile presences (e.g. app or not, responsive or not), something to be expected in this early phase as all companies start to grow up in this area. One thing to be aware of course is both the ever increasing demands that customers have, partly driven by innovation in other sectors, a theme I’ll cover shortly.

2. MEASURABILITY REMAINS A PROBLEM FOR RETAILERS, WITH SMARTPHONE GROWTH INCREASING THE COMPLEXITY HERE

Returning to Google’s IRX presentation, their 3rd main point was to “Be Measured” and this constant striving for better analytics and measurement to aid improved decisions was unsurprisingly a key theme from just about everything I heard and discussed at IRX. Of course, this quest for improved data and insights is also not new, but the continuing march of the smartphone is making this more complex to measure as well as changing many previously established dynamics. For example, Paul Goldstein from Google stated that 90% of consumers use multiple screens when buying online, but the established “last click wins” model is still highly prevalent and the main success metric for the majority of retailers, so many optimise to this. The old ROPO model (research online, purchase offline) has been with us a while but the complexity of measuring this accurately, and then being able to utilise this data in a meaningful way to optimise marketing activity, has long been the holy grail for retailers. Google stated that 59% of customers researched online before their last in store purchase: an impressive stat that is likely lost in standard day to day digital marketing programmes. With the importance of digital (and Google AdWords of course!) often under-reported, Google have been developing further ways to track both cross devices and in store purchases. It was reported that advertisers using Google's cross-device insights are measuring up to 16% more conversions as they benefit from a much wider picture than just tracking a customer on one laptop for example. Even bigger uplifts were mentioned when looking at digital influence on store purchases, with retailers using Google Store Visits data (to help tie up the online and physical) being able to measure 4 times more overall conversions that were started digitally, and a huge 10 times more when looking specifically at mobile.

Unsurprisingly, it is not just Google amongst the internet’s giants that is looking to help retailers understand this influence (and ultimately shift even more media spend to digital channels). For example, Facebook last month announced a partnership with Tesco owned Dunnhumby to help FMCG brands understand the impact of Facebook campaigns in store at the supermarket. It’s probably safe to say that despite making progress around marketing attribution, the industry overall has still not solved the issue of how to fully measure and assess the importance of all customer touchpoints. With mobile growing in importance (but often further up the funnel and thus not measured via the common “last click wins” method), this will be key for retailers to understand and advertising providers to help them get there. Easier said than done of course, especially with the complexity of the marketing technology landscape as I blogged about in March.

3. IS ECOMMERCE UX INNOVATION BEING LEFT BEHIND BY OTHER SECTORS?

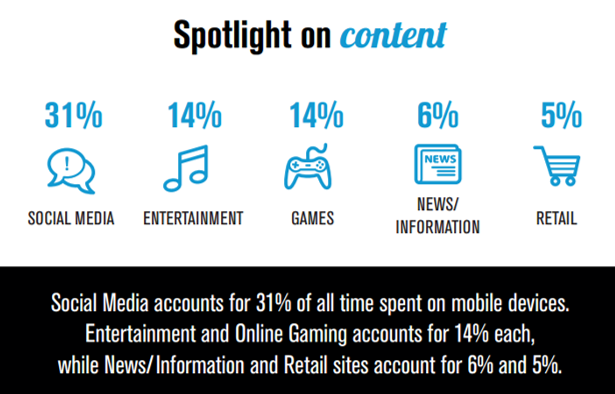

With all this complexity to consider (measurability, multiple channels) plus the aforementioned 20 years of history to fall back on, is it possible that ecommerce is being left behind in the UX stakes by new nimbler, truly mobile first experiences as varied as Instagram, Uber, messaging services such as WhatsApp/Facebook Messenger and even Tinder? With shopping only accounting for 5% of time spent on mobile, these new interfaces are becoming the smartphone norm for customers who may not see the difference between buying a pair of shoes or a lamp with ordering a taxi or even looking for love.

Smartphone users spend the majority of their time on social media and other entertainment. Source: Comscore (June 2015)

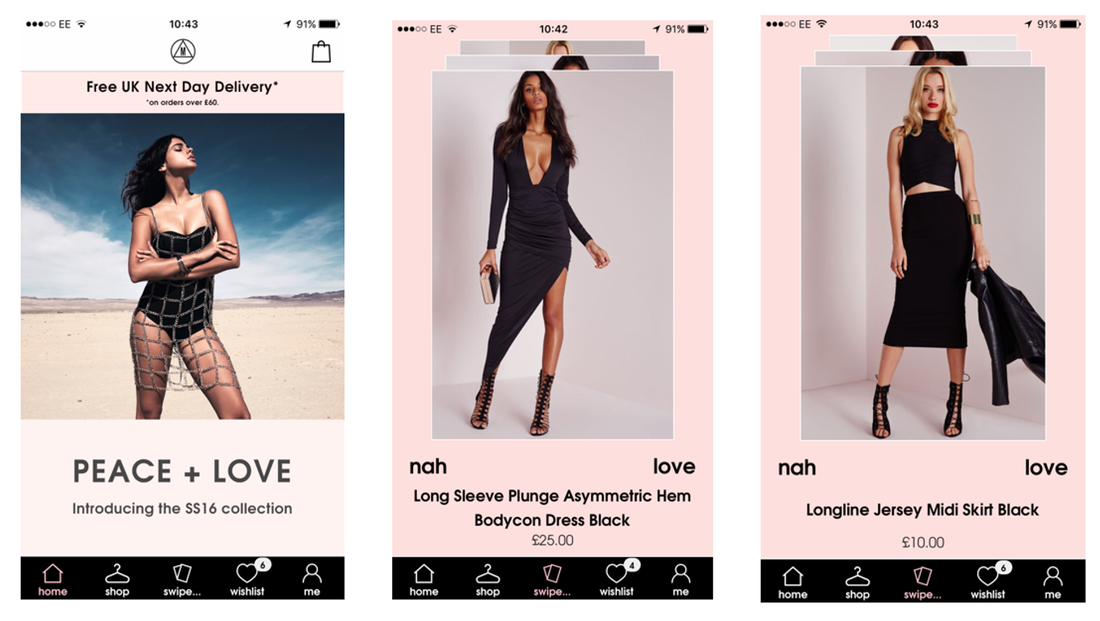

As an example, Tinder’s hugely simple interface is starting to provide inspiration for some fashion brands, such as Missguided, whose mobile app includes a “swipe to hype” feature clearly modelled on Tinder’s swipe left/right functionality. This allows you to build your own wish list based on a constant flow of different clothing options, alongside more standard ecommerce features, albeit even these benefit from a design that feels akin to Instagram, seemingly a wise move for this brand’s young female demographic. Of course, this type of experience will not be suited to many retailers, but it does serve as a good example of challenging traditional UX hierarchy and looking wider than just competing ecommerce sites for inspiration.

Sample screens from Missguided's mobile app, including its Tinder inspired "Swipe to Hype" section

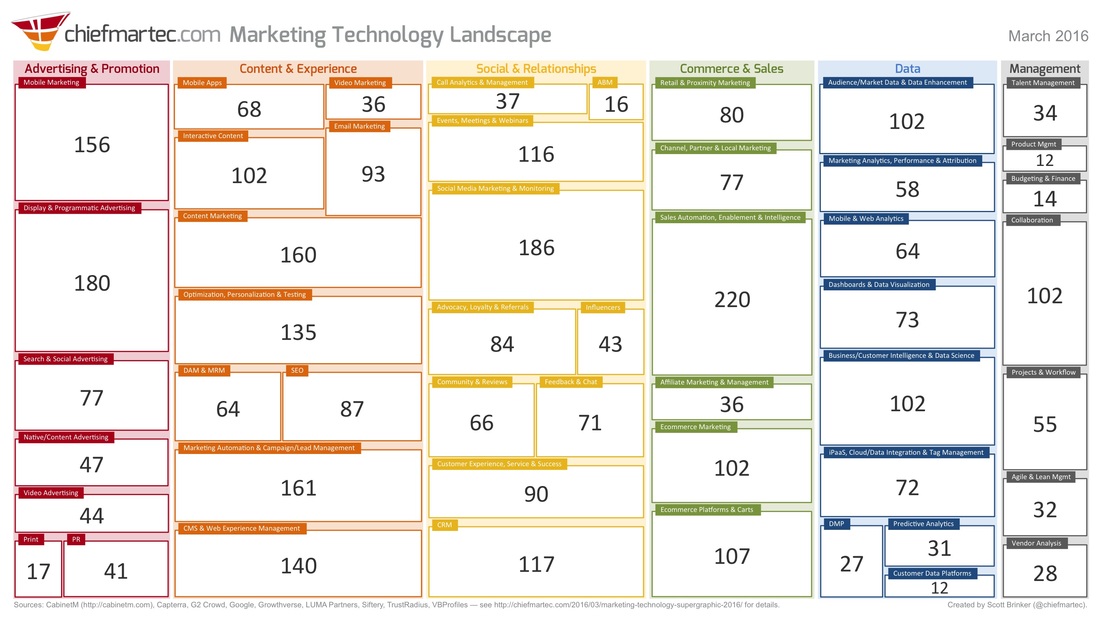

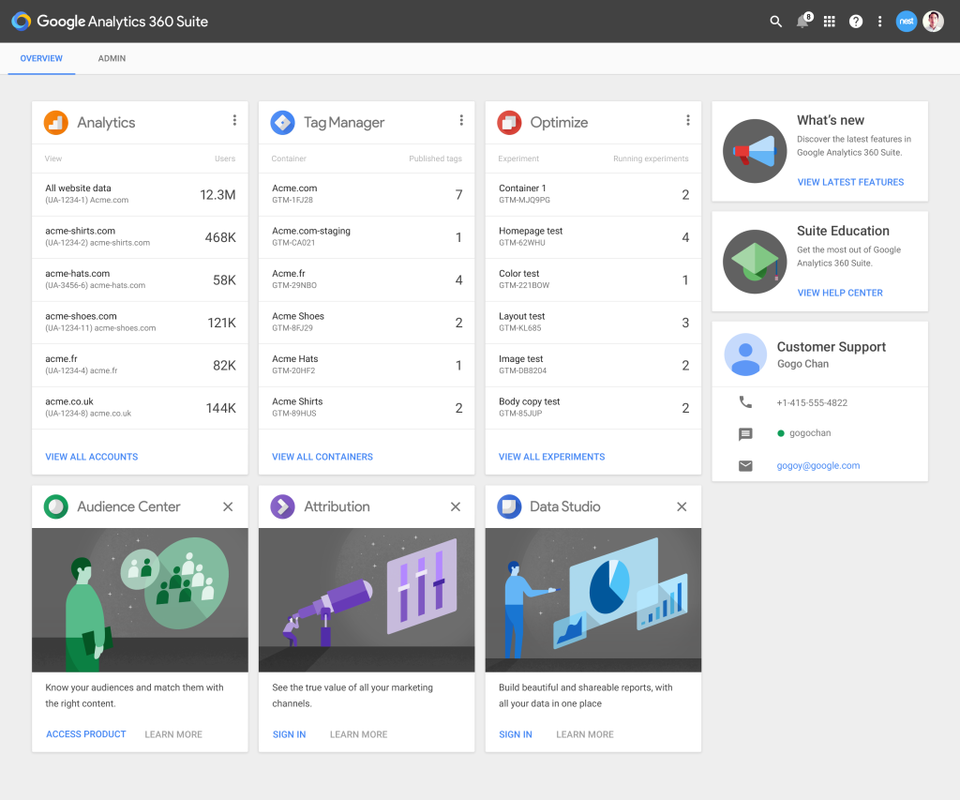

So, in conclusion, a really stimulating day at IRX with much food for thought. It feels like the world of internet retailing continues to move forward as ever, with a real aspiration to true omni-channel capabilities. The issue of measurement continues to be a challenge (and probably always will), but a challenge with real upsides for those able to streamline their data sets into actionable insights. However, the smartphone space will remain the biggest growth priority by far for most ecommerce operations. Here, it is the different opinions and challenges faced by many retailers, coupled with the need to keep abreast of wider mobile trends and innovations, which means that mobile strategy will no doubt continue to occupy the majority of forward thinking in the coming 12 months. This week, Scott Brinker issued his updated Marketing Technology Landscape for 2016. Now an extremely helpful and anticipated annual review of this sector, it is perhaps no surprise that this year’s super graphic is bigger than ever – although a doubling of marketing technology solutions shown to 3874, from 2015’s 1876 (itself double the 947 featured in 2014) is maybe unexpected, and certainly not what I personally predicted in December when looking ahead to 2016. This blog looks at the key developments compared to last year’s landscape and pulls out my 3 main takeaways, including a look at Google’s newly announced Analytics 360 Suite.  Scott Brinker’s Marketing Technology Landscape Supergraphic (2016): click on image to download as a PDF As Scott’s accompanying blog post makes clear, this continuingly large increase in solutions seems to have come about because rather than moving to a “one platform to rule them all model”, many organisations continue to use multiple platforms in their marketing technology stacks, with increasing ease of integration (including a category of products known as iPaaS = integration platforms as a service) meaning that the “all in one” solution is not as crucial to provide consistent data integration/customer experience etc as may have been believed before. NB – Of course, one other reason for the increase may of course be the ever growing industry interest in Scott’s landscape itself, with every tech solution no doubt making sure they are represented on there this year! One of the most interesting parts of the update is changes in how the multiple vendors are categorised, no simple job on such a huge chart. Here, I have to say that I really like the 6 categories that have been used for 2016, which are focused on 6 marketing technology capability clusters (with multiple categories then underneath):

These new clusters appear more consistent with the final customer experience compared with last year’s model where marketing experience and operations solutions were “stacked” on top of infrastructure and platform systems at the bottom. This new set-up sees clusters 1-4 helping to replicate a typical customer funnel in logical order, with accompanying Data and Management enablers as numbers 5 and 6. Generally pulling out “paid” marketing as cluster 1, with “owned/earned” living in clusters 2, 3 and 4 is also a really helpful distinction from 2015.  This graphic shows the number of solutions in each category, led by Sales Automation, Enablement & Intelligence with 220. So what does all this mean? Here are my 3 key takeaways from this new Marketing Technology Landscape… 1. JOINING THE DOTS AND PLUG & PLAY SUPPORT ARE NOW THE NORM As alluded to above, I think it is significant that “Integration Platforms As A Service” (or iPaaS) has been pulled out as its own category, including data integration and tag management solutions. As our consumer lives via iOS, Android etc have become increasingly simple and user friendly, so marketers have been demanding a similar level of flexibility with business technologies. The huge 2016 landscape shows how big this potential system is overall.  2. BUT THE BIG BEASTS AREN’T GOING ANYWHERE However, of course base platforms do remain fundamentally important as core building blocks, with the significant recent news here being Google’s announcement last week of Google Analytics 360 Suite. With Google Analytics Premium at its core, this will consist of existing Google tag management and attribution products as well as other new applications. These include a new data visualisation tool Data Studio 360, Optimise 360 (on site testing and personalisation) and Audience Centre 360, a data management platform. An obvious challenger to the likes of Adobe’s Marketing Cloud and similar services from IBM, Salesforce etc – it will be interesting to see how this develops in the coming months.  3. THE NEW CLUSTERS SEEM CLOSER TO TYPICAL MARKETING PLANNING, THEREFORE MAKING IT EASIER TO ASSESS TECH REQUIREMENTS As I mentioned above, it is instructive that “paid” marketing channels are in a separate cluster to “owned/earned”, which I feel is particularly important for the hugely broad sphere of a discipline like content marketing, which now is well represented in cluster 1 (via “native/content advertising” and “video advertising”), cluster 2 (well, pretty much all of it as this cluster is “Content & Experience") plus cluster 3 (e.g. “Social Media Marketing”). In essence, what this does help to demonstrate is that for any successful campaign, ultimately to be serviced by cluster 4 “Commerce & Sales”, it is likely that a combination of channels from the first 3 clusters will be used. But of course, not all – and when developing any marketing tech stack, it is those priority calls about what to focus on when you can’t do everything that are always key. And finally, many thanks to Scott Brinker for producing this always helpful and thought provoking graphic. Although there is by necessity a lot packed in there, it is really useful as a “50,000 foot overview of the entire space”. There are various links to the original landscape through this blog, but you can also visit Scott’s website at www.chiefmartec.com |

Jim ClearLead blogger and founder of Clear Digital: talking about ecommerce, digital, marketing and media.

Categories

All

Archives

December 2020

|