Today’s Clear Digital Digest round-up looks at:

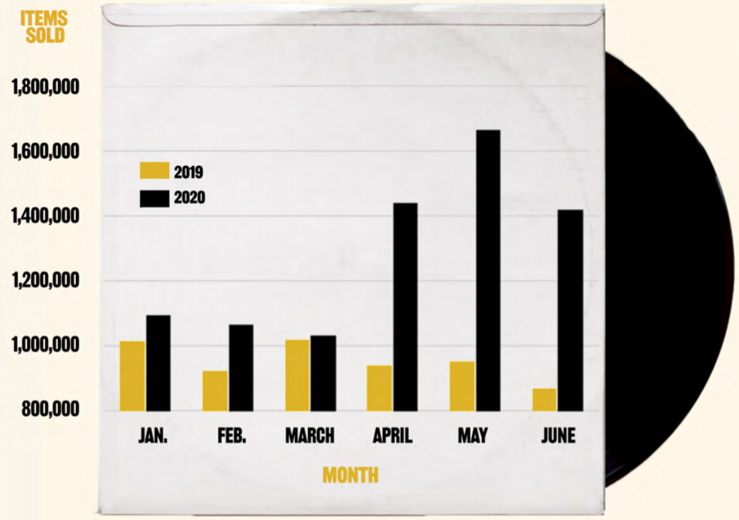

OCADO LAUNCHES WITH MARKS & SPENCER: PERCY PIGS FOR ALL (WELL, SOME…)  Ocado launched their much publicised partnership with Marks & Spencer on Tuesday (Percy Pig branded vans et al) and with such a highly anticipated launch, perhaps unsurprisingly there were teething troubles as some disgruntled customers were not happy that their day one orders were cancelled. Those of us who have been around the block won’t be surprised that there were one or two problems with a new service launch, and time will tell how short-term or significant these issues were. However, Ocado chief executive Tim Steiner was perhaps bullishly tempting fate the weekend before when he told the Sunday Times: “They [Waitrose] have done an advert saying ‘we’ll take it from here’ or something. Well, they can’t take it from here because they don’t have the technology, the infrastructure or the systems.” “Taking it from here” referred to the fact that previous Ocado partners Waitrose were already running their own parallel Waitrose.com delivery service, generally despatched from local Waitrose stores rather than Ocado’s regional distribution hubs. Waitrose also recently announced plans for a 12 week trial with Deliveroo, joining brands such as Morrisons and the Co-Op already on the platform in selected locations. Sainsburys also continue to expand and promote their similar new ChopChop service, as the choice and variety of grocery home delivery options expands to keep up with this year’s step change in customer demand. VINTAGE/USED ITEMS CONTINUE TO DRIVE SALES ON EBAY AND DISCOGS There were two updates from key marketplaces this week, both showing the increasing appetite for vintage/second hand items, a trend we explored in much more depth in our recent deep dive on “The UK Marketplace Sector – And The Role Of Community”. eBay UK have stated that sales of used goods jumped 30% between March and June this year leading to an overall 10% rise in the first half of 2020 compared with last year. Secondhand and vintage fashion is by far their biggest category, but sales of secondhand chairs, sofas and TVs also shot up by 41%, 30% and 17% respectively during June and July compared with February and March. Music community Discogs (the 10th most visited marketplace in the UK) have also released their mid-year report this week. In the first six months of 2020, 4.3m orders were placed globally through the Discogs marketplace (+30% year on year) for a total of 7.7m items (+34% YOY). Vinyl records remain by far the largest sellers for Discogs, with 5.8m sold (+34% YOY) although CD sales also grew by a similar amount, with 31% YOY growth for the 1.7m sold.  Total items sold by month on Discogs H1 2020 v 2019 (Source: Discogs) As the chart above shows, Discogs sales growth really accelerated as lockdown fully kicked in around the world, although January and February were already showing healthy sales growth. This is in line with more recent trends for Discogs, who sold a total of 14.6m records in 2019, growing by 34% on 2018. We explored the Discogs marketplace – and the community that underpins it – in more detail in our recent deep dive “Discogs: The Digital Success Story Of The Vinyl Revival”. NETFLIX TRIALS FREEMIUM  Netflix this week revealed plans to offer some of its original movies and shows to non-subscribers. Free films available include Bird Box and The Two Popes, while original series include Stranger Things and Our Planet. The real hook to this new initiative is the fact that it’s only the first episode of each show that is available, although Netflix newbies can still get a month’s free trial to then continue watching. This type of freemium model seems to make perfect sense for a lower risk trial for anyone that hasn’t yet succumbed to Netflix’s charms; as we reported last month, 43% of UK households currently subscribe to Netflix, ahead of Amazon Prime Video’s 35%. A full list of “free” Netflix shows and movies is available here. AND FINALLY... In a week when the future of another certain Argentinian footballing genius remains up in the air, this tweet raised a chuckle (and makes perfect sense with the final touch)…

0 Comments

It’s now been 5 months since we entered lockdown and then slowly started to re-emerge as restrictions began to ease, bit by bit. It would be trite to say the world has changed in a way previously unrecognisable to all of us; of course it has and constantly so. In fact the pace of change makes it increasingly difficult to keep up, especially with a seemingly never-ending deluge of data and information and data being provided. Looking at these awful events from an ecommerce perspective, I’ve highlighted 5 key trends from these last 5 months to help understand the seismic shifts we’ve been experiencing with regards to how customers have been shopping during this unique period:

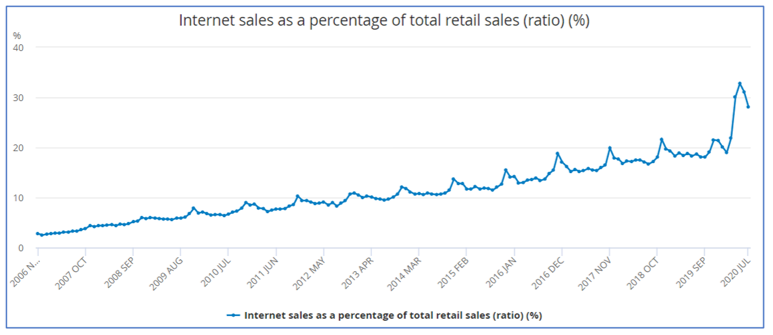

This Clear Digital Digest takes a look at each of these trends in turn, as well as providing some retro gaming light relief at the end… 1. ONLINE SALES HAVE ACCOUNTED FOR AS MUCH AS A THIRD OF TOTAL RETAIL SALES DURING LOCKDOWN This insightful chart from the Office for National Statistics (ONS) shows the huge growth in ecommerce sales during lockdown, with internet sales peaking at 32.8% of all retail sales in May.  Source: ONS

2. ECOMMERCE DROVE £658M OF ADDITIONAL GROCERY SALES JUST LAST MONTH

According to Nielsen’s head of retailer and business insight Mike Watkins:

3. SUCH DYNAMIC ECOMMERE GROWTH IS SPEEDING UP SECTOR INNOVATION This step change in customer behaviour is seeing a never faster pace of innovation within the market, with recent developments including:

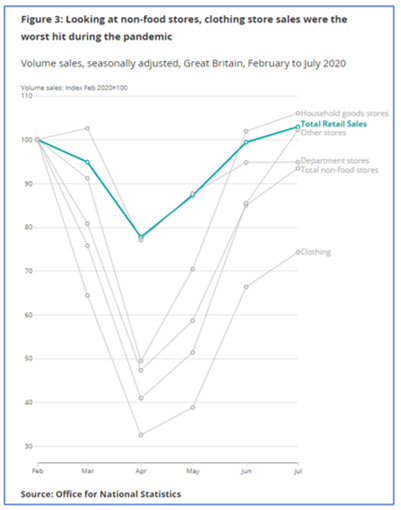

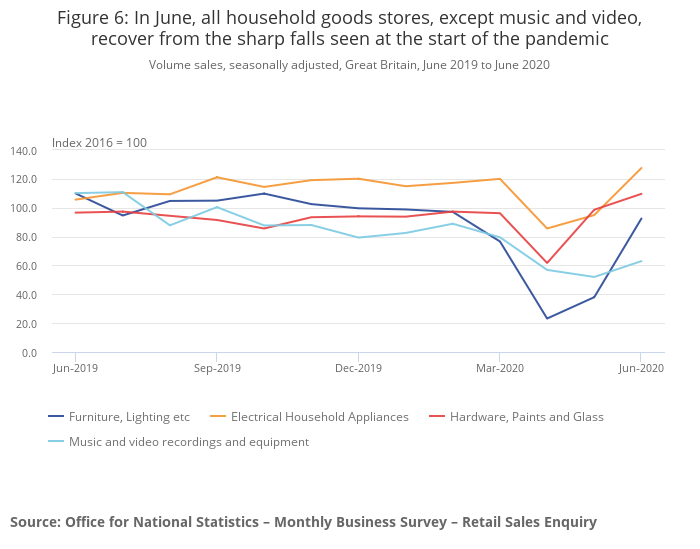

4. SPENDING IS VERY SQUEEZED IN OTHER SECTORS, ESPECIALLY CLOTHING AND MID-MARKET BRANDS

5. AS WELL AS ECOMMERCE INNOVATION, OTHER NEW CHANNELS ARE BEING INTRODUCED, SUCH AS PRODUCT RENTAL

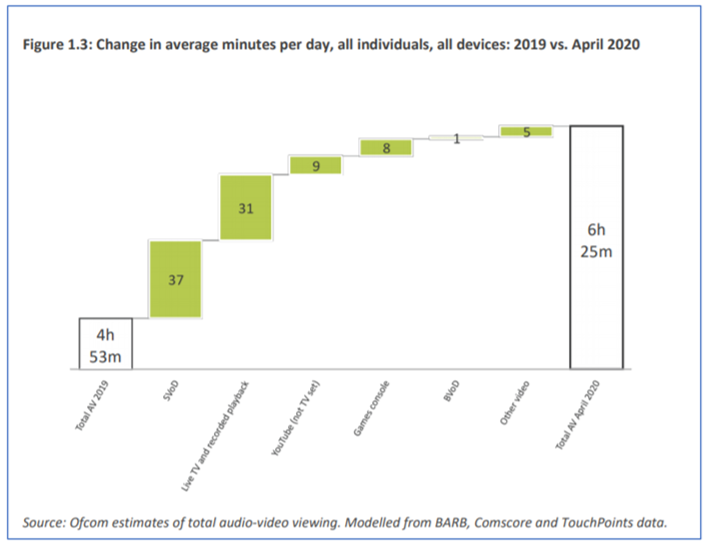

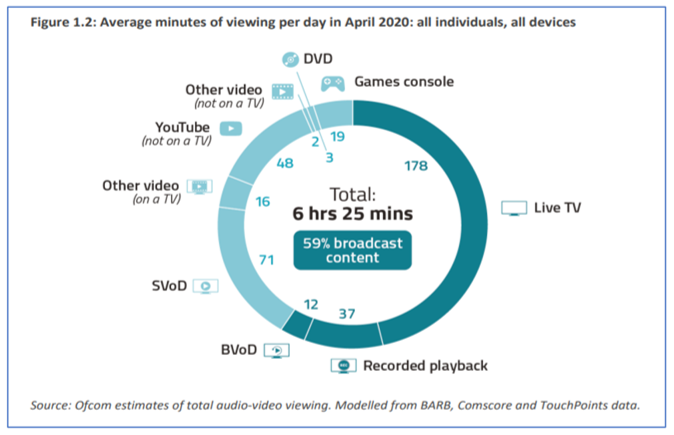

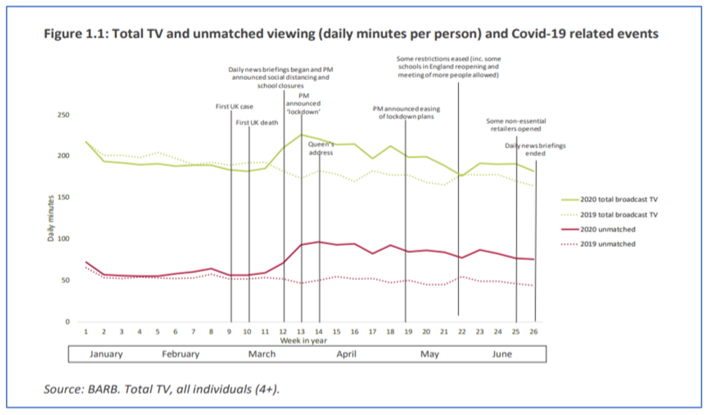

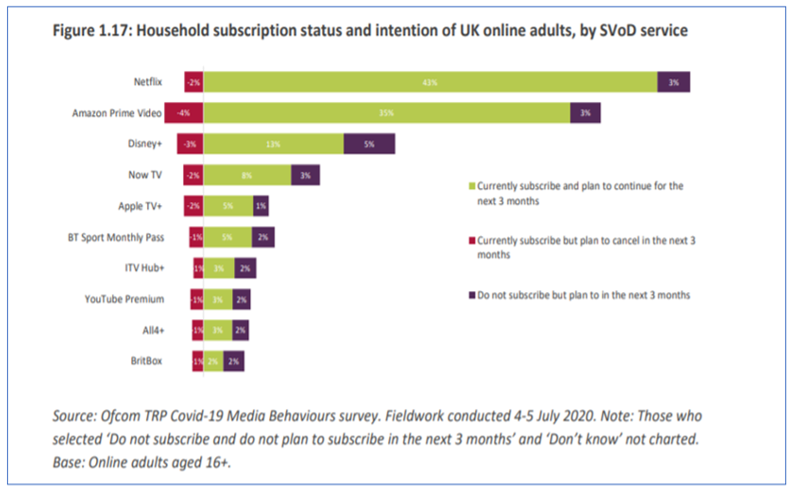

AND FINALLY… As an 80s kid that loved arcade gaming and a 90s student who used part of his student loan to buy a Sega Mega Drive, before then becoming involved professionally as a PS2/Xbox buyer in the 00s, I really enjoyed watching the new Netflix video games history docuseries “High Score” - well the first two episodes I have thus far encountered anyway…  Today’s Clear Digital Digest reviews a recent Ofcom report about our changing TV and video viewing habits since lockdown. We also take a look at changes in the ecommerce world, covering both shopper attitudes plus news from Amazon, Aldi and the mooted return of a familiar old retail brand, Comet… CHANGING VIEWING HABITS Ofcom have just released their latest annual Media Nations research report, examining how we consume TV, video, radio and audio content. This year’s events have unsurprisingly seen quite significant changes since March, so Ofcom have added two chapters to their report examining Covid-19 related trends. Some key highlights from this are:

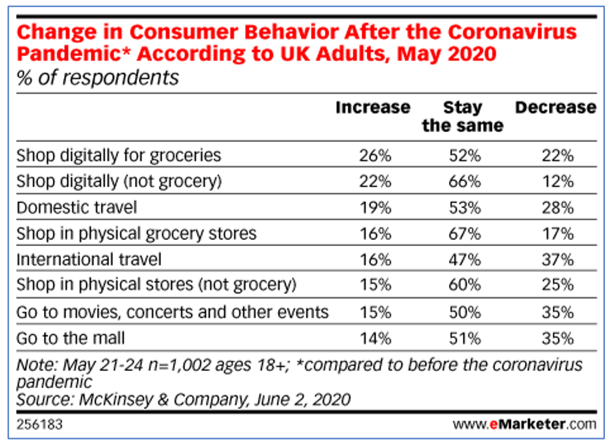

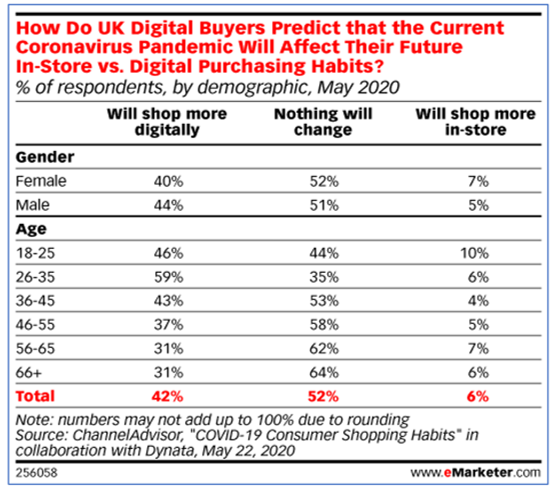

CHANGING SHOPPING HABITS As well as changing our viewing habits, Covid19 has also fundamentally changed our shopping habits with the well documented growth in online shopping. eMarketer have taken a look at what these shifts may mean in the longer term.

Looking at other ecommerce stories, a week never seems to go by without some significant Amazon news and the last seven days are no exception.

Today’s Clear Digital Digest reviews a recent survey on changing customer attitudes as well as the latest IPA Bellwether marketing spend report. The MP3 is 25 years old this week and although not widely used these days, as the key tech that paved the way for streaming its influence can often be understated, as we explore below. Plus a look across the Channel at a new, unique way to watch films… CONSUMER ATTITUDES AND MARKETING SPEND Amongst the latest insights that emerged this week, Wunderman Thompson’s “Covid, Commerce and the Consumer” report stood out, based on a survey of 2000 UK consumers in early June. Some key highlights include:

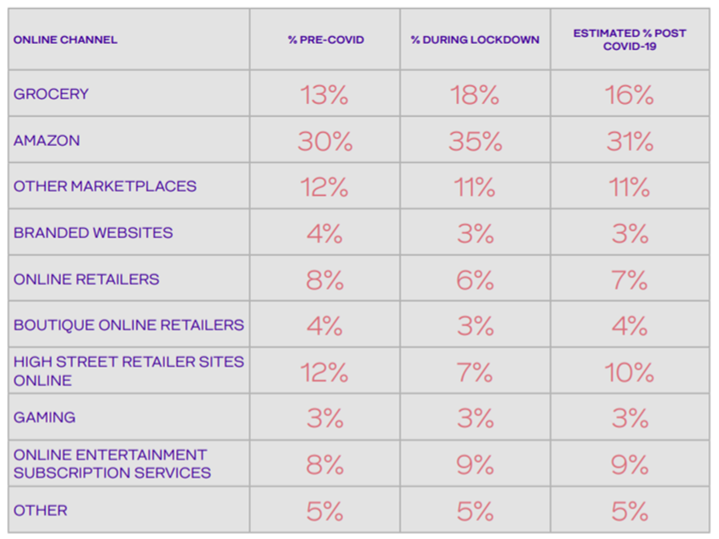

Estimated lockdown % online shopping share, source: Wunderman Thompson

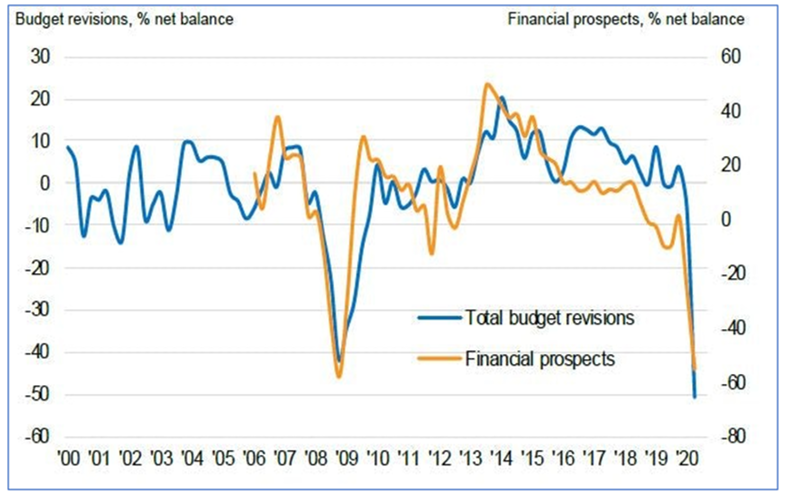

IPA Bellwether Report, source: IPA/Marketing Week MP3 TURNS 25 There was an important but fairly unheralded digital milestone this week, as the MP3 file turned 25.

AND FINALLY... With cinemas closed until recently and only gradually re-opening now, one new trend has been the emergence of drive-in cinemas to bring some US retro flavour to cinephiles who are seeking more than another Netflix binge. Venues as varied as Brent Cross Shopping Centre car park and Alexandra Palace will be accommodating such yearnings this summer. However, Haagen-Dazs are adding a new flavour in Paris with their “Cinema Sur L’Eau” concept: a socially distanced cinema where customers will sit in boats rather than cars. Further investigation reveals they will be showing a film entitled Le Grand Bain (English title: Sink Or Swim), about a group of men who start their own synchronised swimming team. Certainly a wiser choice of movie to show in this environment than Jaws or Titanic.   It’s now just 3 weeks to go till Euro 2016 kicks off in France on Friday 10th June, and while the tournament itself will have some way to go in order to match the still incredible story of Leicester City’s domestic Premier League triumph, the extra home nation interest this year will undoubtedly see passion levels run high once Euro 2016 actually starts. Summer football events such as the Euros are now also an established part of the marketing and promotion calendar for many brands – for both official sponsors and other companies – so I’ve taken a look at how some of them have so far embraced this opportunity. It was estimated that the 2014 World Cup contributed £2.5bn to UK consumer spending and it is believed that Euro 2016 will generate a similar amount, with food, drink, retail and betting sectors seeing the greatest benefits. Over 60% of pubs are predicting like for like sales increases of more than 10% through June, with the England v Wales group match on Thursday 16th June unsurprisingly highlighted as a particularly large opportunity.  Pubs are expecting a significant sales uplift during Euro 2016. Source: Morning Advertiser/MatchPint The nature of big sporting tournaments like Euro 2016 lends itself to a variety of different objectives for brands, in particular:

OFFICIAL SPONSORS: CARLSBERG EARLY PACE-SETTERS UEFA have 10 official sponsors for Euro 2016; ranging from the usual suspects such as Adidas, Coca-Cola and McDonalds to emerging brands which won’t be as familiar to European consumers. These include the Chinese consumer electronics company Hisense and the seemingly aptly named Socar. Socar is actually the State Oil Company of the Azerbaijan Republic, so in reality this organisation is perhaps not such a natural fit for football tie-ins as Carlsberg for example.  Amongst official sponsors, Carlsberg have certainly been to the fore with their activation plans, with a range of initiatives all following the “if Carlsberg did…” strapline, seemingly both in domestic markets and pan European too. This week, Carlsberg have been trailing online a new ad campaign starring Marcel Desailly, one of France’s World Cup 98 and Euro 2000 winning heroes. “If Carlsberg Did La Revolution” will undoubtedly feature heavily in June during TV coverage, with many hidden references in there for football geeks as well. Amongst the standard ticket giveaway competitions, Carlsberg have also been using more creative methods ahead of the tournament in the UK, including Chris Kamara looking at what would happen “if Carlsberg did substitutions” and rewarding generous Tube travellers with tickets to the Euros. Other UK focused campaigns include experiential activity, with Carlsberg rebranding 19 English pubs as the patriotic “The Three Lions”. Some other selected highlights from official sponsors include:

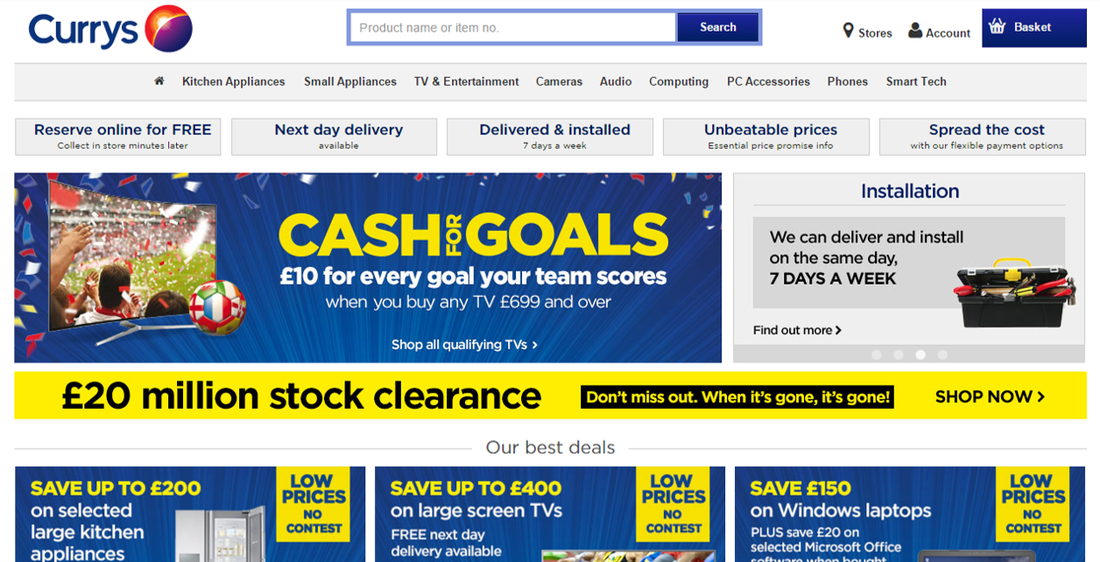

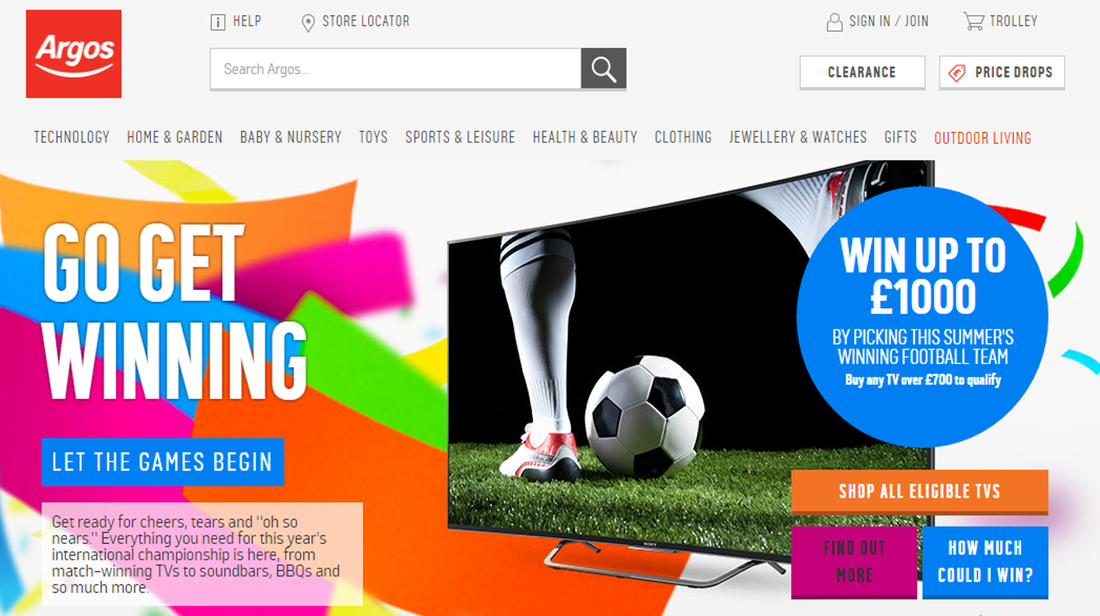

“UNOFFICIAL” CAMPAIGNS: PREDICT THE WINNER 3 weeks out and it may be a bit early to stock up on essentials like food and drink if planning a barbecue party, but it is the perfect time for more considered purchases to enhance your Euro 2016 viewing pleasure, such as a shiny new TV. And full disclosure here: I did once buy a new TV in time for Euro 2004, so this does actually happen! However, with governing bodies such as UEFA monitoring and protecting their trademark rights to enhance the aforementioned sponsorship deals, this tends to result in some creative descriptions by the vast majority of brands that are not filling UEFA’s coffers; leading to the use of many generic campaign titles such as the “summer of sport" rather than the trademarked "Euro 2016" or similar. A couple of good examples here are provided by Currys and Argos, both of whom are offering TV promotions with a prediction element based around "this summer’s big football tournament" (aka Euro 2016).  To the fore on Currys’ homepage is their “Cash for Goals” promotion, backed up by a range of accompanying media both online and offline. This is a deal that Currys have run in similar form during previous summer football tournaments, and means that should you spend over £699 on a TV, Currys are offering £10 cashback for each goal that either England, Wales, Northern Ireland or Republic of Ireland score during the tournament. Customers can pick their team and with more choice amongst British Isles teams than usual, it will certainly be interesting to see if customers patriotically pick their own home nation, or go for another team based on their perceived chances.  Argos are also focusing on upper end TVs by offering customers a chance to win up to £1000 by “picking this summer’s winning football team” when you buy a TV over £700 in their “Go Get Winning” promotion. Further investigation shows that for those heartened by the Leicester fairytale, you can win £1000 back if you plump for an outsider like Albania or Slovakia (or Northern Ireland/Wales), down to £100 for France, Germany or Spain. An England win, unlikely as it may seem, would net you £250 cashback. AND FINALLY… As well as official Euro 2016 sponsors maximising their activity with glossy campaigns and giveaways, plus retailers looking to sell appropriate seasonal products, multi-national sporting events generally also see a few more esoteric tie-ins as well. Expect to see some of these to the fore as the tournament approaches, but as a tasty example, the Amazon listing below provides some food for thought…  What's the most popular British TV programme? And what other big event is on the horizon? These Euro 2016 cake toppers provide an ideal baking/football mash-up |

Jim ClearLead blogger and founder of Clear Digital: talking about ecommerce, digital, marketing and media.

Categories

All

Archives

December 2020

|